Beware: existing customers always pay higher interest rates

Investopoly

Banks will usually offer higher interest rate discounts to new customers to win their business. But, of course, the banks never offer these higher discounts to existing customers, unless they ask for them.

Whilst this has always been the case, it is noteworthy that interest rate discounts have increased substantially over the past 10 years. This means the gap between what interest rates existing and new customers are being charged has also widened to the extent that it is becoming more important that you (or your mortgage broker) review your loans at least annually.

New customers are enjoying higher discounts

A decade ago, interest rate discounts (i.e., discount off the standard variable rate) typically ranged between 0.70% and 0.90% p.a. Today, we are obtaining discounts of up to 2.95% p.a.[1]! This means it’s very likely that new customers are paying significantly lower interest rates than existing ones, particularly if they haven’t renegotiated their loans for a few years.

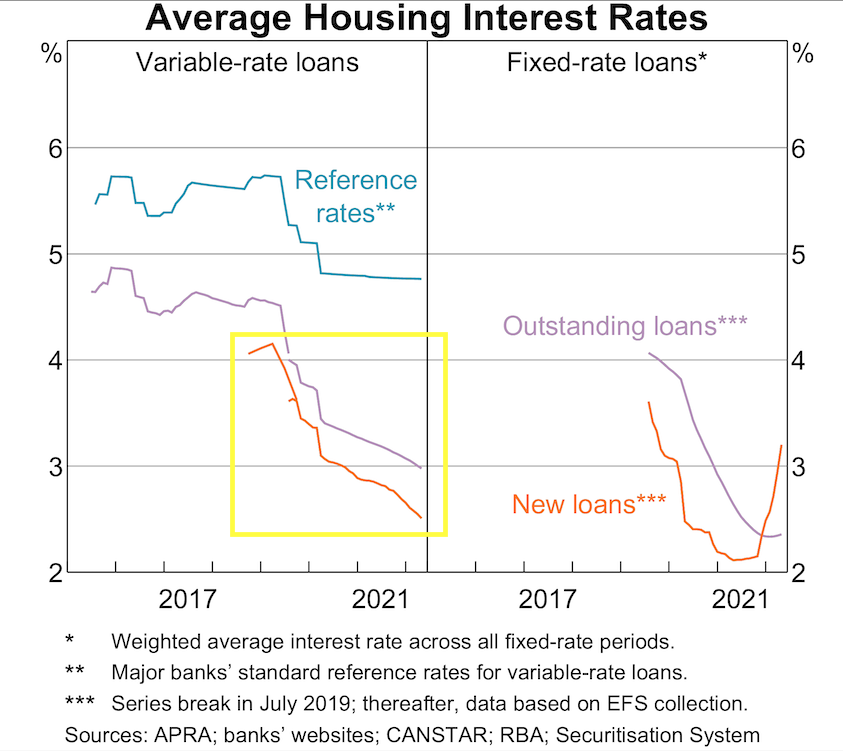

The chart below is compiled by the RBA and illustrates that new customers (orange line) are, on average, being charged lower variable interest rates than existing customers (purple line) – see yellow highlighted box. As you can see, this gap has widened considerably over recent years.

What drives home loan discounts?

Management remuneration packages (i.e., senior banking executives) tend to be linked to shareholder returns i.e., the share price. Bank share prices will be affected by factors such as (1) growth in mortgages compared to their peers and (2) net interest rate margin (which essentially is the gross profit generated by mortgage lending). A positive or negative change in these factors will tend to have an influence on a banks’ share price.

For a variety of reasons, banks can experience phases where they produce better results (i.e., high growth and margins) than their peers. Conversely, the reverse is true too. Therefore, when a bank underperforms, it must make up for lost growth and buy a greater share of the (mortgage) market. It does this through discounting, either through broad based promotions or more often, offering higher customer-specific discounts to win new business.

For example, in its recent half-yearly presentation in May 2022, Westpac confirmed that its investment mortgage loan book experienced a decline of 6.6% since September 2020 whereas its competitors, such as CBA, maintained its level of investor lending. Therefore, it is not surprising that Westpac is now offering higher interest rate discounts to win new investment loan customers.

All the banks ebb and flow between being more and less aggressive regarding pricing (discounting) which creates useful competition for proactive borrowers and mortgage brokers.

Automated re-pricing of mortgages

At ProSolution, we have recently implemented an artificial intelligence tool that periodically re-prices our clients’ mortgages. Using a range of data, it calculates what variable interest rates our clients should be paying and then automatically submits a request to their lender/bank to match that pricing.

With the growing popularity of fintech, I’m sure it won’t be long before similar tools to be available to consumers.

What to do if you don’t have a mortgage broker

It is advisable to proactively review your loans if your mortgage broker doesn’t do that on your behalf (or you don’t have a mortgage broker).

To do that, you must first research which lenders will offer you the highest discount. That will depend on many factors including your LVR, total lending, number of individual loans, whether you have any exist

Our most popular free guides:

Over the years we've written hundreds of articles. These three bring our best thinking together on the topics that matter most right now: choosing a super fund, debt recycling, and navigating the new tax changes.

My new book, Wealth by Design, is out now:

Buy online or in bookstores. The ebook is available now, audiobook coming soon.

Got a question for the podcast?

Email us at questions@investopoly.com.au

Interested in working with our team?

Discover how we can work together

Subscribe to my weekly blog:

Important

This podcast provides general information about finance, tax and credit. It doesn't take into account your specific objectives, financial situation or needs, so you need to assess whether it's relevant to your circumstances before acting on it. If you're not sure, speak to a licensed, trustworthy professional.

{kind=link}