Brace for a big drop in consumer spending in 2023

Investopoly

As you are aware, the RBA has aggressively hiked rates by 3% p.a. over the past 8 months, so variable home loan rates are now more than 5% p.a. (and investment loans approaching 6% p.a.). Fixed rate borrowers have avoided these higher interest rates. However, a lot of fixed rates will begin expiring next year. As such, many borrowers are facing much higher (40%+) mortgage repayments next year.

These higher interest rates will have a huge impact on consumer discretionary spending and economic growth in 2023.

Many Australians have accumulated large liquidity buffers

Many Australians have enjoyed vastly improved cash flow during covid lockdowns as interest rates were at all-time lows (e.g., fixed rates were sub-2% p.a.) and people couldn’t spend money on their usual leisure activities. Australians did two things with their improved cash flow.

Firstly, they directed some of this cash flow towards improving liquidity buffers such as repaying home loans and/or accumulating cash in offset and savings accounts. According to RBA data, household savings (deposits) grew by over $500 billion (or 21%) since the beginning of the pandemic until June 2022. It is noteworthy that household liabilities have increased by only 12% over the same period.

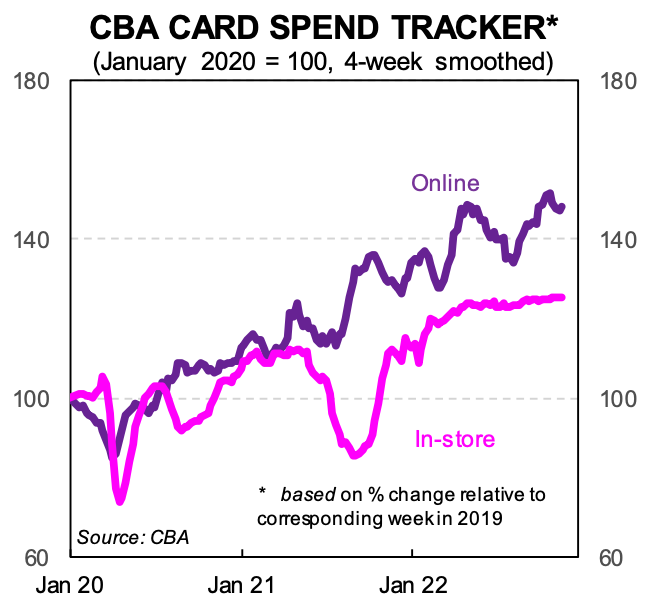

Secondly, they spent more money on discretionary items. As the chart below from CBA illustrates, during lockdowns, Aussies would spend online and return instore once lockdowns were lifted – Covid didn’t adversely affect spending.

This chart covers the period from January 2020 until the end of November 2022. Total spending is still over 30% higher than it was at the beginning of 2020, although spending on things like retail and eating out has declined over recent months.

Discretionary spending will be the first to be cut

Faced with the decision of whether to eat out or pay the mortgage, of course virtually everyone will choose to meet their liabilities first.

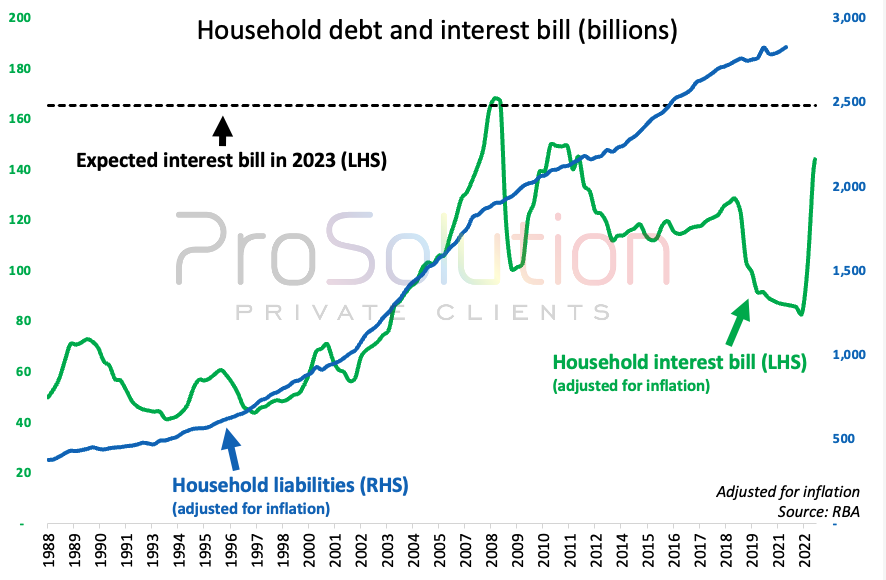

The chart below illustrates the interest cost of mortgages assuming all mortgages were on variable interest rates (of course, many are fixed, as discussed above). The black dotted line is the projected total household interest bill at the current cash rate of 3.10% p.a. i.e., once all the rate hikes have been passed on. As you can see, once the cheap covid fixed rates expire, interest costs will be the same as they were pre-GFC in 2008 (in real terms). That is likely to have a massive impact on discretionary spending.

Most borrowers will be ok

I don’t expect a large increase in mortgage default rates. Most borrowers have been tested that they can afford to repay rates 3% higher than when they first apply for the loan (rates have now risen 3%). Therefore, so long as there’s not too many more rate hikes, borrowers should be able to afford these higher interest rates. It might not be easy or comfortable, but borrowers will tend to explore all avenues to stay in their family home i.e., not default on their mortgage.

I remind you that savings (including offset accounts) have swelled by 21% over the past couple of years. Once discretionary spending has been cut, I’m sure that many borrowers will need to dip into these savings, which will go a long way.

Of course, there will be some borrowers that have over-borrowed, or their circumstances have changed, and may experience financial stress and must sell their home. But I think these are likely to be in the minority and less likely to be in investment-grade locations.

Don’t wait for a property crash in blue chip areas </

My new book is available for pre-order now: Pre-ordering the book will help me get it into bookstores. So please do me a favour - please consider pre-ordering now - links and pre-order bonus are available here: https://prosolution.com.au/book-preorder-bonus

Do you have a question for the podcast? Email us at questions@investopoly.com.au.

If you're interested in working with our team and me, discover how we can work together here: https://prosolution.com.au/family-office-services

If this episode resonated with you, please leave a rating on your favourite podcast platform.

Subscribe to my weekly blog: https://prosolution.com.au/stay-connected

IMPORTANT: This podcast provides general information about finance, taxes, and credit. This means that the content does not consider your specific objectives, financial situation, or needs. It is crucial for you to assess whether the information is suitable for your circumstances before taking any actions based on it. If you find yourself uncertain about the relevance or your specific needs, it is advisable to seek advice from a licensed and trustworthy professional.

{kind=link}

{kind=link}