What to do if your fixed rate or interest only term is due to expire in 2023

Investopoly

It has been very well reported that many mortgage holders will soon be paying much higher interest rates when their fixed rate terms expire. It is estimated that $478 billion worth of fixed rate mortgages are due to expire in 2023.

In addition, borrowers may also have to navigate the end of an interest only term, which typically apply to investment loans.

This blog sets out our advice on how to navigate these changes.

What are your options?

Fixed rate expiry

If your fixed rate is maturing, you have two options. You can re-fix your interest rate for another term or allow the interest rate to roll over onto a variable rate.

Current fixed rates range between 5.39% and 6.10% p.a. for owner-occupiers and 5.69% to 6.70% p.a. for investors (terms between 2 and 5 years). Variable interest rates range between 4.75% to 4.90% p.a. for owner-occupiers and 5.30% to 5.50% p.a. for investors on interest only repayments. As such, fixed rates don’t look attractive for a couple of reasons.

Firstly, it is very likely that we are at or close to the top of the interest rate cycle. So, there’s limited value in paying a premium (i.e., a higher interest rate) to protect yourself against potentially higher interest rates in the future.

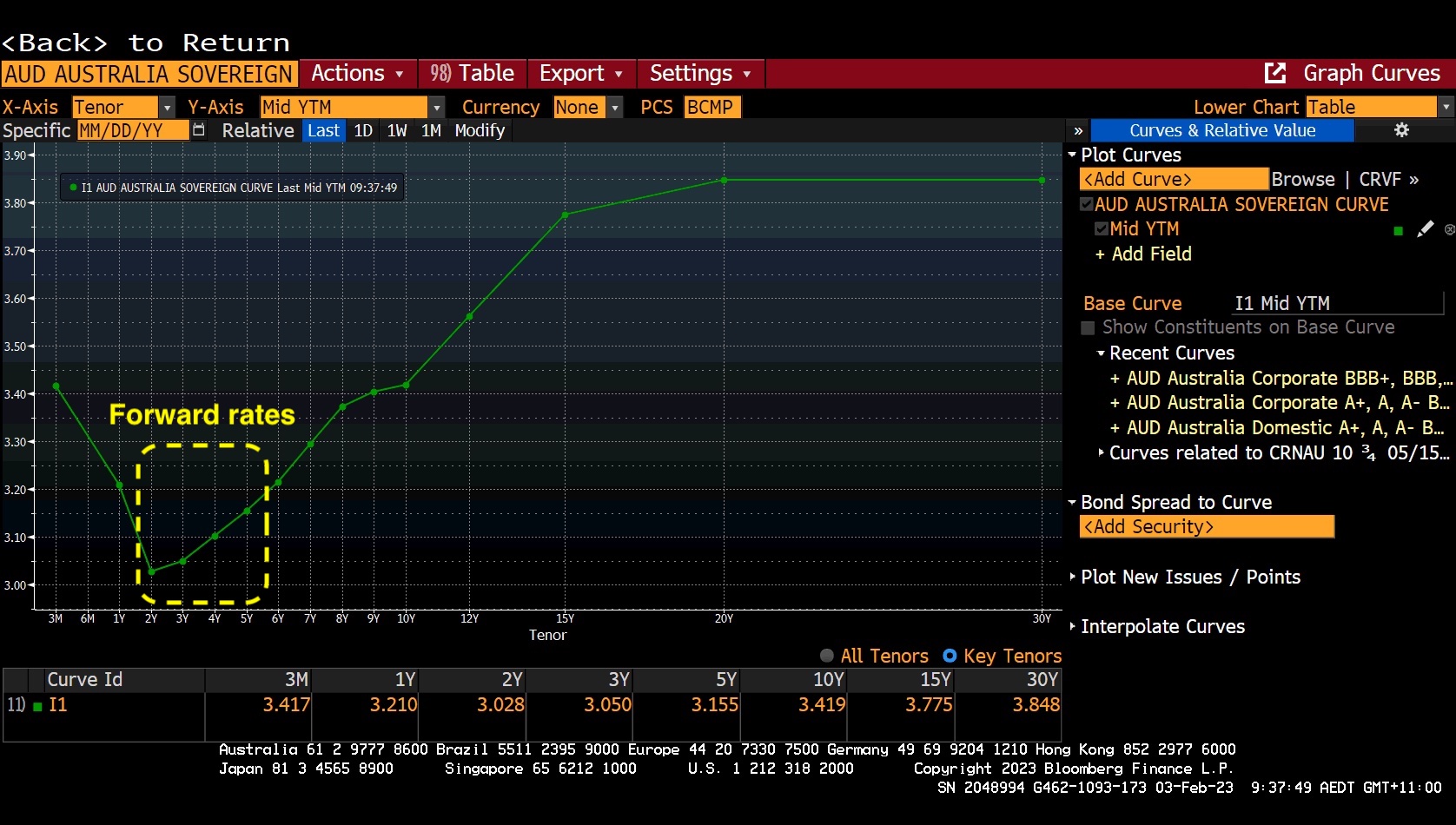

This chart shows that the interest rate yield curve over 5 years is relatively flat i.e., it implies that RBA’s cash rate won’t change much over the next 5 years. Fixed rates may become attractive again when/if the yield curve inverts because it reduces the banks term borrowing costs and allows them to offer more attractive fixed rates. Until that happens, we typically recommend rolling over onto a variable interest rate.

Interest only term expiry

Navigating an interest only term expiry is not always straightforward. Usually, all mortgages have 30-year terms. If you elect to initially repay interest only, your loan term typically consists of a 5-year interest only term plus a 25-year principal and interest term. Contractually, the bank doesn’t have to offer you another interest only term – they can insist that you repay principal and interest for the remainder of the loan term. You have two options; request another interest only term or agree to repaying principal and interest.

There are two common matters you should consider being (1) cash flow and (2) interest rates.

The advantage of repaying interest only is that you minimise your monthly commitment. You might want to do that either because you want to divert cash flow elsewhere such as repaying your (non-tax-deductible) home loan or so that you can take advantage of an offset account, as explained here.

The downside to interest only loans is that they attract higher interest rates. In 2017, the banks began charging higher interest rates for interest only loans to dissuade borrowers from requesting them (at the time the banking regulator was concerned that 40% of new loans were interest only). Interest-only loans attract a higher interest rate of 0.26% p.a. (on average) compared to principal and interest investment loans (or a 0.55% p.a. premium for interest only home loans) – that is the premium you pay during the interest only loan term.

Consider your whole portfolio: some questions to ask yourself

We suggest reviewing your whole mortgage portfolio at one time instead of reviewing loans individually. Doing so ensures that you achieve the best overall outcomes.

When reviewing your loan portfolio, it is wise to consider a few matters such as:

§ Will your borrowing capacity change in the future? A c

My new book is available for pre-order now: Pre-ordering the book will help me get it into bookstores. So please do me a favour - please consider pre-ordering now - links and pre-order bonus are available here: https://prosolution.com.au/book-preorder-bonus

Do you have a question for the podcast? Email us at questions@investopoly.com.au.

If you're interested in working with our team and me, discover how we can work together here: https://prosolution.com.au/family-office-services

If this episode resonated with you, please leave a rating on your favourite podcast platform.

Subscribe to my weekly blog: https://prosolution.com.au/stay-connected

IMPORTANT: This podcast provides general information about finance, taxes, and credit. This means that the content does not consider your specific objectives, financial situation, or needs. It is crucial for you to assess whether the information is suitable for your circumstances before taking any actions based on it. If you find yourself uncertain about the relevance or your specific needs, it is advisable to seek advice from a licensed and trustworthy professional.

{kind=link}