The Insurance Producers Guild

The Insurance Producers Guild is a strategic briefing for insurance professionals, focused on Medicare, ACA, life insurance, and the evolving insurance landscape. Each episode distills complex industry changes into clear, practical intelligence.

The Insurance Producers Guild

EP5 The Compliance Moat - CMS’s $10B Crackdown & Agency Risk

Use Left/Right to seek, Home/End to jump to start or end. Hold shift to jump forward or backward.

In this episode of The Insurance Producers Guild, we break down one of the most significant enforcement actions in ACA history, and what it signals for the future of insurance agencies.

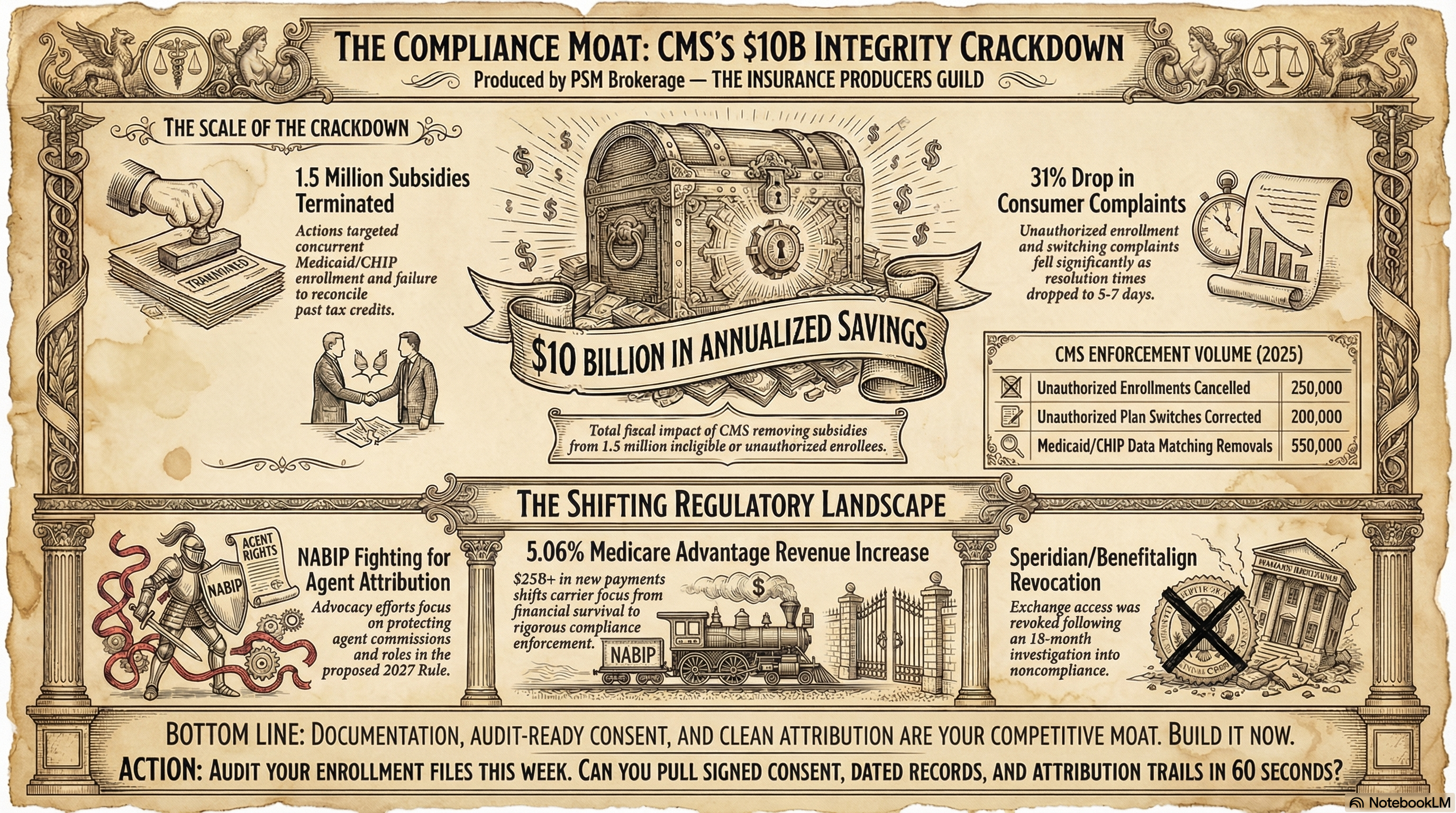

CMS has removed subsidies from nearly 1.5 million enrollees and driven an estimated $10 billion in annualized savings through aggressive Exchange integrity enforcement.

With 250,000 unauthorized enrollments cancelled, 200,000 improper plan switches identified, and complaint resolution timelines compressed to just 5–7 days, the message is clear: compliance is no longer optional, it’s operational infrastructure.

We also examine the high-profile Speridian/Benefitalign enforcement action, where CMS revoked Exchange access after an 18-month investigation, setting a new precedent for accountability across the industry.

At the same time, NABIP is actively pushing back on elements of the proposed 2027 Marketplace rule, advocating to preserve agent attribution, protect compensation structures, and maintain standardized plan options that agents rely on during Open Enrollment.

On the Medicare Advantage side, CMS finalized a 5.06% revenue increase for 2026 and completed the three-year risk model phase-in — creating financial stability for carriers while shifting focus toward operational quality and compliance oversight.

Across both ACA and Medicare Advantage, one theme stands out: the rise of the “compliance moat.” Agencies that invest in documentation, consent capture, and clean attribution will scale, while others face increasing regulatory risk and operational drag.

🔑 Key Topics Covered

- CMS Exchange integrity crackdown and $10B in savings

- 250,000 unauthorized enrollments and 200,000 improper plan switches

- Faster complaint resolution timelines (5–7 days)

- Speridian/Benefitalign enforcement and Exchange access revocation

- NABIP response to the proposed 2027 Marketplace rule

- Agent attribution and compensation protection efforts

- 2026 Medicare Advantage rate increase (5.06%)

- Completion of the MA risk model phase-in

- The growing importance of compliance infrastructure in agency scaling

🎯 What This Means for Agents

- Compliance is now a competitive advantage, not just a requirement

- Documentation and recorded consent are becoming audit-critical assets

- Clean agent attribution directly impacts revenue protection and renewals

- Faster CMS enforcement cycles reduce margin for operational error

- Agencies without strong compliance systems risk losing market access

- Medicare Advantage stability allows agents to focus more on process quality

- Scalable agencies will be defined by how well they operationalize compliance

Infographic:

https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/IPG_EP5%20Infographic.png

{kind=link}

Slides:

https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/IPG_EP5%20Slides.pdf

🔗 Sources

CMS Exchange Program Integrity Fact Sheet (January 2026):

https://www.cms.gov

InsuranceNewsNet / NABIP Comments on Proposed 2027 NBPP (March 2026):

https://www.insurancenewsnet.com

CMS 2026 Medicare Advantage & Part D Rate Announcement (April 2025):

https://www.cms.gov

Learn more: https://www.psmbrokerage.com

The Insurance Producers Guild Podcast delivers intelligence for insurance agents looking to stay ahead of industry trends.

Follow the show and connect with PSM Brokerage to access tools, training, and support designed to help you grow your business.

Learn more: https://www.psmbrokerage.com

You are probably hearing uh the exact same massive rumor that is just tearing through the industry right now.

SPEAKER_00Oh, it's absolutely everywhere. I mean, it is dominating the agency floors.

SPEAKER_01Aaron Powell Right. And honestly, it is causing a lot of sleepless nights. The word on the street is that CMS is aggressively removing health insurance subsidies from well, from one and a half million people.

SPEAKER_00Aaron Powell Which obviously causes immediate panic. Agents are looking at their books of business, just terrified that they might be next.

SPEAKER_01Aaron Powell Exactly. They think they are going to log into their portals tomorrow and just see half their ACA and under 65 commissions completely wiped out.

SPEAKER_00Aaron Powell Well, welcome to the Insurance Producers Guild. Today's operational briefing is all about, you know, separating that fear from the actual facts.

SPEAKER_01Aaron Powell, I mean, I've been through this before, right? But before we get into the patterns of what CMS is doing, we need to uh dissolve that panic immediately. Trevor Burrus, Jr.

SPEAKER_00Stop right there. Because we really do. Context is everything here. CMS is not indiscriminately targeting your book of business. They are specifically surgically targeting bad actors.

SPEAKER_01Right, the ones making a mess of things.

SPEAKER_00Exactly. We are talking about people executing unauthorized enrollments, uh agents intentionally doubling up clients on concurrent Medicaid and exchange coverage, and individuals who are failing to file their taxes.

SPEAKER_01Which is a huge red flag.

SPEAKER_00Yeah. So if you run a clean operation with proper consent documentation, this crackdown is not a threat to you. It is a shield. Trevor Burrus, Jr.

SPEAKER_01And I love that framing. A shield.

SPEAKER_00It actively clears out the unethical players who, frankly, make our entire industry look bad, and it leaves more market share for true professionals.

SPEAKER_01That's a great point. Like I said, I've been through this before. Every few years, CMS tightens the screws. I saw it in the early days of Medicare Advantage, and we are seeing it heavily now in the Affordable Care Act marketplace.

SPEAKER_00Right. The cycle just repeats.

SPEAKER_01Exactly. And agents with clean files, they don't even notice the disruption. But we have a very specific mission for this agency building session. Which is we are going to break down exactly what these new CMS actions and the upcoming 2027 rules mean for your book, your clients, and your commissions.

SPEAKER_00Yes. And more importantly, let me tell you, we are going to give you the exact operational plays to run this week to capitalize on it.

SPEAKER_01So let's look at the hard, verified numbers because the scale of this cleanup is breathtaking. CMS has ended premium subsidies for nearly 1.5 million people on the FFE platform.

SPEAKER_00And for anyone new to the space, the FFE is the federally facilitated exchange. Basically, the healthcare.gov platform that handles enrollment for states that do not run their own state-level exchanges.

SPEAKER_01Right. So when you do the math on removing 1.5 million subsidized individuals from that platform, it results in a staggering $10 billion in annualized savings.

SPEAKER_00Aaron Powell 10 billion. That is just a massive number.

SPEAKER_01It really is. And when you unpack where those removals are actually coming from, you start to really see the pattern of who CMS is going after.

SPEAKER_00Yeah, the breakdown is fascinating.

SPEAKER_01Over one million of those individuals were concurrently enrolled in Medicaid or CHIP, the children's health insurance program, and exchange coverage at the exact same time.

SPEAKER_00Which, you know, you cannot have double coverage like that, heavily subsidized by the government twice. It just doesn't work.

SPEAKER_01Exactly. They broke the removals down for us. So uh 435,000 were caught via Medicaid data matching.

SPEAKER_00Aaron Powell Basically, the state Medicaid systems and the federal exchange systems finally started talking to each other.

SPEAKER_01Aaron Powell Right, exactly. Then another 250,000 were straight up unauthorized cancellations.

SPEAKER_00Wow.

SPEAKER_01Yeah. And 235,000 were removed for failure to file and reconcile their taxes. Which, you know, is a strict legal requirement if you are receiving advanced premium tax credits.

SPEAKER_00Aaron Powell Which means the cleanup is actually working. I mean, CMS noted that consumer complaints have dropped by 31%.

SPEAKER_01That's a huge drop.

SPEAKER_00It is. And their resolution times for these complex enrollment issues are now down to five to seven days. That is a massive operational improvement for them.

SPEAKER_01Aaron Powell, it really is. But here is the critical shift in their enforcement mechanism. They established a new preponderance of the evidence standard for terminating agent and broker exchange agreements.

SPEAKER_00Right. And they also completely eliminated the 150% FPL SFP.

SPEAKER_01Okay, let's pause and translate that because that is a massive change. FPL SA stands for Federal Poverty Level Special Enrollment Period. Right. Historically, if a client's income was under 150% of the federal poverty level, agents could use that special enrollment period to move them into a new plan almost any time of the year.

SPEAKER_00It was meant to help low-income families get coverage outside of the standard open enrollment window.

SPEAKER_01Exactly. But bad actors were using it as a massive loophole for unauthorized switching, flipping clients from plan to plan just to generate new commissions.

SPEAKER_00Yep. And CMS shut that down completely. And they took major enforcement action against Sporidian Technologies, the parent company of Benefit Align and True Coverage, after like an 18-month investigation.

SPEAKER_01Well let's go back to that preponderance of the evidence standard for a second, because I really want to push back on how this is being rolled out.

SPEAKER_00Okay. What do you mean?

SPEAKER_01Well, in the past, CMS had to prove a higher level of intent determining an agent's agreement. They had to prove you were actively trying to defraud the system, but under a preponderance of the evidence standard, they just need to show that it is more likely than not that a violation occurred. That is a much, much lower bar.

SPEAKER_00It is.

SPEAKER_01So I have to ask, um, how exposed are agents who are fundamentally honest, but maybe just a little sloppy with their paperwork? I mean, I know a lot of great agents who are incredible at explaining life and health benefits, but terrible filing clerks.

SPEAKER_00Aaron Powell That is the exact vulnerability right there. And let me give you the exact script and the play you need to run to fix it today.

SPEAKER_01Okay, let's hear it.

SPEAKER_00We call this the 60-second file audit. Here is the play you run right now. If you cannot pull a client file and show a signed consent form, a dated enrollment record, and a clear attribution trail in exactly 60 seconds, you have a massive operational problem.

SPEAKER_0160 seconds. Wow.

SPEAKER_00Stop what you were doing and fix your filing system this week. Because under a preponderance of evidence standard, sloppy documentation looks exactly like intentional fraud to an auditor.

SPEAKER_01That's a really scary thought, but it makes sense.

SPEAKER_00They aren't going to spend weeks trying to figure out if you meant well. If the paperwork isn't there, boom, you lose your ability to sell.

SPEAKER_01That is a stark reality. I mean, if you are fumbling around in four different software programs looking for a text message confirmation from eight months ago while an auditor is just sitting there waiting, you have already lost.

SPEAKER_00Exactly. You need a centralized, immediate way to prove that the client sitting across from you actually asked you to do the work.

SPEAKER_01Is it a timestamped IP address? Is it a recorded phone line snippet? It just has to be accessible. And this connects directly to what we are seeing coming down the pipeline for the future. CMS is cleaning up the mess today, but the proposed 2027 rules could actually erase your ability to get paid tomorrow if you aren't tracking your own attribution independently.

SPEAKER_00Aaron Powell You're talking about the proposed rules for the notice of benefit and payment parameters, right? Yeah. The NBPP for 2027.

SPEAKER_01Aaron Powell Precisely. This is the annual rule book CMS publishes that dictates exactly how the Affordable Care Act markets will operate.

SPEAKER_00Aaron Powell Right. And EBIP, the National Association of Benefits and Insurance Professionals, which represents, what, over 100,000 licensed agents? They just submitted their formal comments on this rule book.

SPEAKER_01Aaron Powell They did. And the major threat they are highlighting is the expansion of the Enhanced Direct Enrollment Pathway or EDE. Trevor Burrus, Jr.

SPEAKER_00Yeah, that's a big one. For those heavily utilizing technology to enroll clients, EDE is a system that allows private websites and broker portals to complete ACA enrollments without the client ever having to visit healthcare.gov directly.

SPEAKER_01Right. And under the proposed expansion of this EDE pathway, an agent could do all the heavy lifting, you know, guide a client through the complex network options, explain the deductibles, finalize the application, and end up with absolutely zero record of their involvement in the system.

SPEAKER_00Aaron Powell Because the software could literally strip your national producer number, your NPN, off the application due to how the data is routed.

SPEAKER_01Exactly. Think of it like a real estate agent.

SPEAKER_00Okay.

SPEAKER_01Imagine you find the perfect house for a buyer. You spend weeks showing them properties, you negotiate the price, you handle all the inspection paperwork, and you finally get them to the closing table. Right. But the moment the title company's software processes the deed, a technical glitch automatically erases your name from the transaction so the seller doesn't have to pay your commission fee. Oh, that would be brutal. You did all the work, the buyer got the house, and you walked away with nothing because the system didn't track your attribution. That is exactly what NABP is warning could happen with this ED expansion.

SPEAKER_00Aaron Powell Which means you lose the commission entirely, you did the work, the client gets the coverage, and your agency gets nothing.

SPEAKER_01Yep.

SPEAKER_00And to compound that, CMS is also proposing the elimination of standardized plans in 2027.

SPEAKER_01Aaron Powell, which is another huge operational hurdle. Right now, standardized plans force insurance carriers to offer policies with identical deductibles, out-of-pocket maximums, and co-pays within a specific metal tier. Trevor Burrus, Jr.

SPEAKER_00So a standardized silver plan from carrier A looks very similar structurally to a standardized silver plan from carrier B.

SPEAKER_01Exactly. Makes quoting fast. But NABP is warning that removing standardized plans is going to dramatically increase consumer confusion. Oh, without a doubt. Clients won't be able to easily compare apples to apples anymore. Every single policy will have a completely unique cost-sharing structure. That adds a massive amount of workload to the agent's desk. You are going to have to spend 45 minutes explaining the variations in these plans instead of 15 minutes.

SPEAKER_00And NAP's stance on all this is crystal clear. You know, do not treat agents as presumptively suspect. They are demanding evidence-based enforcement and due process protections for the agent community.

SPEAKER_01Which is incredibly important.

SPEAKER_00But from an agency building perspective, this is a pure monetization and technique issue. If you're not tracking enrollments with independent documentation that proves you initiated the transaction, you're exactly one platform change away from losing your commissions.

SPEAKER_01You cannot rely on the carrier's portal or the government's exchange to be the sole record of your book of business. You have to own the data. So how does an independent agent actually verify that their workflow is bulletproof when the technology is shifting this fast?

SPEAKER_00Well, this is where PSM brokerage comes in. Their compliance team can review your workflow right now to ensure your documentation proves your attribution.

SPEAKER_01Oh, that's huge.

SPEAKER_00Yeah, you want an outside set of eyes on your process before the 2027 rules take effect. If you are using a CRM or a quoting tool, PSM Brokerage's compliance team can look at how you capture consent and ensure that a CMS or a carrier comes knocking, your NPN is definitively tied to that client interaction.

SPEAKER_01I agree with that approach completely. It is fantastic that NIBP is fighting the good fight in Washington for agents who do it right. We need that advocacy.

SPEAKER_00We do.

SPEAKER_01But as an agency owner, you cannot wait for policy to save you. You have to build your compliance moat right now. If you control the documentation, you control your business. It is that simple.

SPEAKER_00100%.

SPEAKER_01And frankly, this focus on compliance isn't just an ACA marketplace issue. We are seeing the exact same pattern materialize in the Medicare Advantage space, but for a slightly different reason.

SPEAKER_00Yeah, the Medicare Advantage landscape is fascinating right now because it has just entered a period of intense financial stability. And financial stability for carriers instantly changes how they treat agents.

SPEAKER_01Let's look at the math on that. CMS just announced a positive 5.06% average revenue change for MA plans in 2026.

SPEAKER_00Which is massive.

SPEAKER_01When you apply that to the entire Medicare advantage market, that is injecting over $25 billion in increased payments into the system. Okay, walk us through it.

SPEAKER_00You start with a massive 9.04% effective growth rate, but then you have offsets pulling that number down. There is a negative 3.01% revision from the risk model, a negative 0.69% from star ratings changes, and a negative 0.28% from rebasing.

SPEAKER_01Right.

SPEAKER_00But the most important piece of news buried in that announcement is that the three-year phase in of the 2024 CMSHC risk adjustment model is now 100% complete.

SPEAKER_01And for anyone not deep in the actuarial weeds, HCC stands for hierarchical condition category.

SPEAKER_00Right.

SPEAKER_01It is essentially the scoring system CMS uses to predict how much health care a specific Medicare beneficiary will need based on their health conditions. A sicker patient gets a higher risk score, which means CMS pays the Medicare Advantage plan more money to cover that person.

SPEAKER_00Makes sense.

SPEAKER_01A few years ago, CMS completely overhauled the scoring system to remove certain codes and change how conditions were weighted. They phased this massive change in over three years so carriers wouldn't go bankrupt overnight. Now that phase in is completely done.

SPEAKER_00That is the pattern right there. For the last three years, carriers have been operating under massive transition uncertainty. They were dealing with changing risk scores, fluctuating payments, and a very difficult macro environment.

SPEAKER_01Wait, let me stop you there. Because I've been through this before with carriers. If I'm an agency owner, my first instinct when carriers finally stabilize and get a 5% revenue bump is that they are going to pay higher commissions or maybe relax their oversight a bit. They have more money, so the pressure should be off. Why would they pivot to aggressively auditing agents just when things are getting good?

SPEAKER_00It's a great question. And it really comes down to protecting the asset. When carriers are fighting for financial survival, that's all they look at. They are just trying to keep the lights on and manage their medical loss ratios. Right. But with this 5% revenue increase and the risk model phase in completely finished, they finally have payment certainty. They know exactly how the math works now. And when carriers have payment certainty, they take those resources and invest them heavily into quality control.

SPEAKER_01Ah, I see.

SPEAKER_00They want to ensure the business staying on their books is pristine so they don't jeopardize that newly stabilized revenue stream.

SPEAKER_01Aaron Powell So when the house is on fire, you don't worry about dust on the baseboards. But the fire is out, the revenue is stabilized. Now they're gonna look very closely at the quality of the business being submitted. They are gonna look at your consent to contact forms, your scope of appointment timing, and your call recordings.

SPEAKER_00Precisely. But rather than viewing this as a negative, you have to frame this carrier audit shift as a massive competitive advantage. Think about the field.

SPEAKER_01Okay.

SPEAKER_00While your competitors are panicking, complaining on social media, and reacting defensively to this new compliance pressure, you are already clean. Because you listened to this briefing and you already ran the sixty-second file audit on your own agency. You already centralized your documentation.

SPEAKER_01So you are saying that operational excellence actually becomes a magnet for the best carrier relationships, that we can use compliance as an offensive strategy to gain market share while the rest of the industry is scrambling to clean up their messy files.

SPEAKER_00Let me give you the exact reality of how this plays out. Let's say you have two agencies submitting 50 applications a month.

SPEAKER_01Okay.

SPEAKER_00Agency A has a 15% error rate, missing signatures, and vague attribution. Agency B can produce a flawless audit trail for every single policy in under 60 seconds. Because your operation is tight, like agency B, you become exactly what the top carriers want.

SPEAKER_01Right. They want to partner with agencies that do not represent a compliance risk.

SPEAKER_00Exactly. And PSM brokerage's contracting support helps you get appointed with these exact carriers, the ones who are actively rewarding clean, tight operations with better support and better opportunities. You leverage your compliance as a selling point to the carriers.

SPEAKER_01It is the ultimate differentiator. Who do you think the carrier's regional vice president is going to invite to the exclusive training events? Who gets the dedicated support representative? Agency B, every single time.

SPEAKER_00Without a doubt.

SPEAKER_01And it goes beyond just carrier relationships. It protects you from the regulatory shifts we talked about earlier. Whether it is CMS sweeping the ACA exchanges for bad actors and saving $10 billion, or NABP fighting to ensure the ED pathways don't erase your hard work. The foundational defense is always the exact same. Document your interactions. Prove your value.

SPEAKER_00It's why I am so adamant about that 60-second rule. I want you to literally run this drill tomorrow morning with your staff. Pick a random client from last Tuesday. Start a stopwatch. Say, show me the signed consent, the dated enrollment, and the attribution.

SPEAKER_01I love that.

SPEAKER_00If the stopwatch hits a minute and they're still clicking through folders, you have your primary operational objective for the week. Fix it. That is what top-tier agencies do. And if you need help navigating which carriers value that level of professionalism, PSM Brokerage has the contracting support to get you positioned correctly in the market.

SPEAKER_01It's measurable, it's immediate, and it removes all the ambiguity. As we wrap up this operational briefing, I want to leave you with a final concept to mull over. Think about the long game here. Having an airtight 60-second auditable file doesn't just protect your commissions from CMS today. It actually acts as a massive multiplier on the valuation of your agency if you ever decide to sell your book of business down the line. Clean books sell for a premium. Buyers don't want to acquire compliance liabilities. They want to acquire guaranteed verifiable revenue streams. Your filing cabinet today is your retirement fund tomorrow.

SPEAKER_00That's this Wednesday's The Insurance Producers Guild. Stay tuned for the next episode. If you're not already with PSM Brokerage, this is the kind of actionable intelligence our agents get. Talk to us about contracting.