The Insurance Producers Guild

The Insurance Producers Guild is a strategic briefing for insurance professionals, focused on Medicare, ACA, life insurance, and the evolving insurance landscape. Each episode distills complex industry changes into clear, practical intelligence.

The Insurance Producers Guild

EP6 The Great MA Benefit Squeeze

Use Left/Right to seek, Home/End to jump to start or end. Hold shift to jump forward or backward.

In this episode of The Insurance Producers Guild, we unpack one of the most disruptive shifts the Medicare Advantage market has seen in over a decade, what we’re calling - “The Great MA Benefit Squeeze.”

Drawing from new analysis by KFF, Johns Hopkins, and Milliman, we explore how slowing enrollment growth, rising healthcare costs, and structural payment pressures are reshaping the entire landscape for 2026.

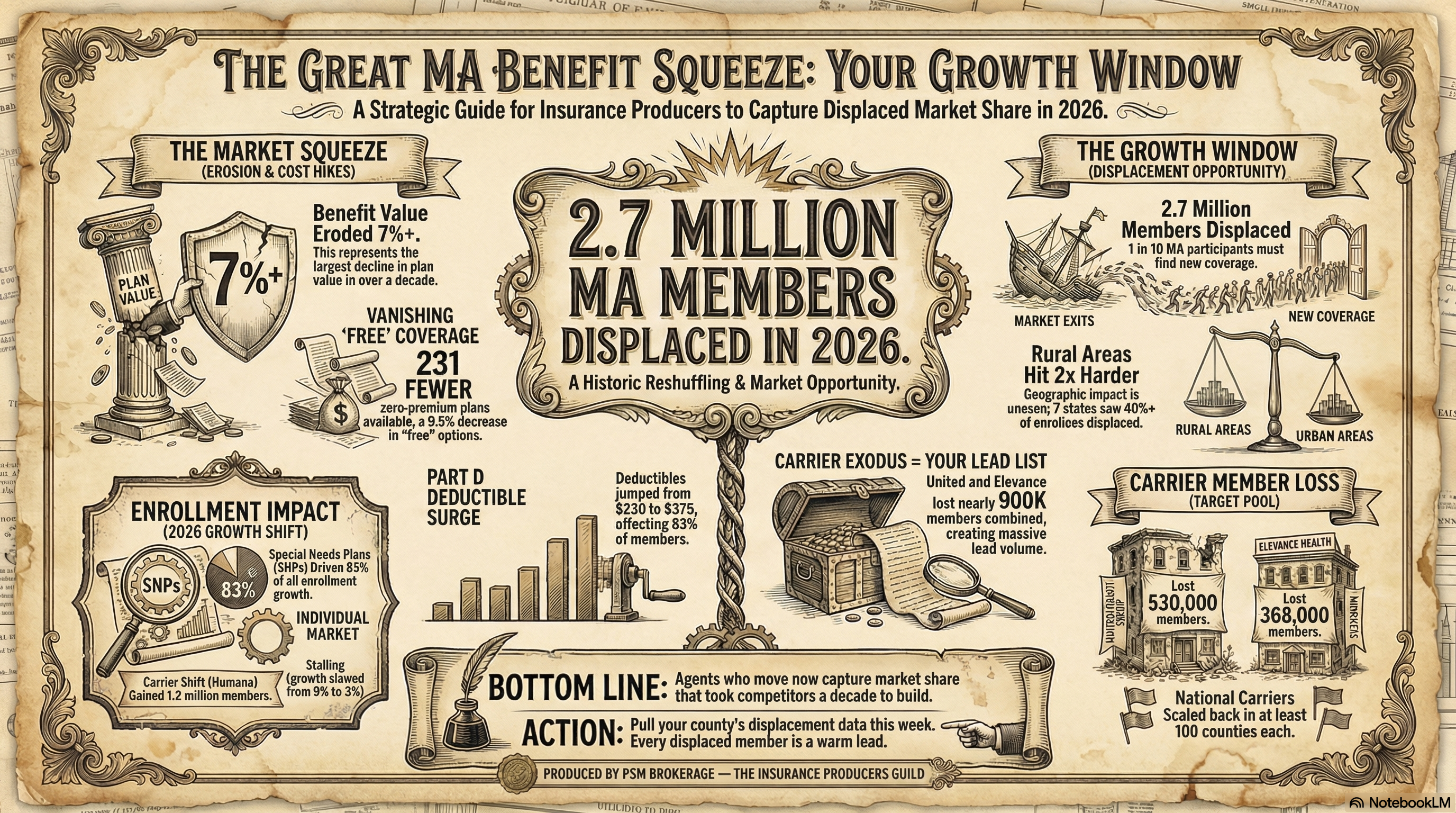

From the explosive rise of Special Needs Plans (SNPs) to the mass displacement of nearly 3 million beneficiaries, the market is undergoing a fundamental transformation. At the same time, remaining enrollees are facing a quieter but equally impactful shift: shrinking benefits, disappearing $0 premium plans, and sharply rising Part D deductibles.

This episode breaks down the “why” behind these changes — and more importantly, what they mean for agents navigating client conversations in a volatile and fast-changing environment.

If you’re still approaching Medicare Advantage with a “set it and forget it” mindset, this episode will challenge that assumption and help you rethink your strategy heading into the next enrollment cycle.

🔑 Key Topics Covered

- Medicare Advantage enrollment slowdown and market saturation

- The rapid growth of Special Needs Plans (SNPs) and shift to high-need populations

- Carrier market disruption: gains, losses, and regional competition

- Why major insurers are losing members despite scale and resources

- The 2.9 million beneficiary displacement crisis for 2026

- Rural market challenges and the economics of provider access

- PPO plan declines and network contraction trends

- “Benefit shrinkflation” and declining plan value

- Elimination of $0 premium plans and what it signals

- Sharp increase in Part D deductibles and member cost exposure

- How actuarial pressures are reshaping plan design and benefits

🎯 What This Means for Agents

- Auto-renew is no longer a safe strategy — every client’s plan must be actively reviewed

- Mass displacement creates a major opportunity to serve high-intent shoppers

- Benefit reductions require agents to shift from plan selection to gap analysis

- Supplemental products (dental, vision, hospital indemnity) become critical tools

- Clients will need help understanding new out-of-pocket exposure, especially drug costs

- Rural markets present both challenges and high-urgency opportunities

- Value conversations must replace “$0 premium” selling strategies

- Agents who can explain why plans changed — and offer solutions — will stand out as trusted advisors

Infographic:

https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/IPG_EP6_Infographic.png

Slides:

https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/IPG_EP6_Slides.pdf

{kind=link}

🔗 Sources

KFF Medicare Advantage Data & Analysis

Johns Hopkins Bloomberg School of Public Health Research

Milliman Actuarial Analysis

The Insurance Producers Guild Podcast delivers intelligence for insurance agents looking to stay ahead of industry trends.

Follow the show and connect with PSM Brokerage to access tools, training, and support designed to help you grow your business.

Learn more: https://www.psmbrokerage.com

So in twenty twenty six, roughly one in ten Medicare Advantage patients will uh well they'll just open their mail to find out that their healthcare plan has simply vanished.

SPEAKER_00Aaron Powell Yeah. Just completely gone.

SPEAKER_01Aaron Ross Powell Right. And in states like Vermont, that number is actually uh 92 percent.

SPEAKER_00Aaron Powell Which is just a staggering statistic to even wrap your head around.

SPEAKER_01Aaron Powell It really is. And today, we are looking at this massive stack of incredibly dense, incredibly urgent reports from KFF, uh Johns Hopkins Bloomberg School of Public Health, and Milliman. And it's all regarding the 2026 Medicare Advantage landscape.

SPEAKER_00Aaron Powell Right. Because if you are navigating this market right now, you know something is up.

SPEAKER_01Aaron Powell Exactly. Whether you are an industry professional trying to salvage a client's coverage or you know just a family member staring down your parents' new out-of-pocket costs, you are dealing with the system experiencing a massive, unprecedented reshuffling.

SPEAKER_00Aaron Powell A total upheaval, yeah.

SPEAKER_01So our mission today for this deep dive is to decode exactly what is going on. We are going to figure out the mechanisms behind why benefits are suddenly shrinking, why millions of people are losing their plans, and uh what this once-in-a-decade upheaval means for your strategy moving forward.

SPEAKER_00It is great to be here to unpack this with you because when you actually dig into the underlying data and you know the math from these reports, it reveals this dramatic shift in how healthcare is going to be delivered in America. Aaron Powell Right.

SPEAKER_01This isn't just small stuff.

SPEAKER_00Aaron Powell Exactly. We aren't just looking at minor policy tweaks here. We are looking at structural, tectonic shifts in the private Medicare market. The numbers we are about to go through are staggering, and they literally touch every single aspect of the industry.

SPEAKER_01Aaron Powell Okay, let's unpack this because the general narrative for years, I mean, it's always been that Medicare Advantage is this unstoppable juggernaut.

SPEAKER_00Aaron Powell Well, for sure. Year after year of massive growth.

SPEAKER_01Aaron Powell Right. It felt like every single year, more and more people were leaving traditional government Medicare to sign up for these private plans. But reading through the KFF data, it seems like that narrative has just fundamentally fractured.

SPEAKER_00Aaron Powell It really has.

SPEAKER_01So can you lay out the baseline of what the market looks like right now just to set the stage for everyone?

SPEAKER_00Aaron Powell Absolutely. So the KFF data shows that total Medicare Advantage enrollment is now just over 35 million people. Aaron Powell Wow.

SPEAKER_0135 million.

SPEAKER_00Yeah. And to put that in perspective, that means 54% of all eligible Medicare beneficiaries have chosen a private Medicare Advantage plan over traditional Medicare. Trevor Burrus, Jr.

SPEAKER_01So this is officially the majority of the country now.

SPEAKER_00It is the majority. But here is the critical data point. The overall growth of the market has hit a massive wall. It has slowed down to just 3% year over year.

SPEAKER_01Aaron Powell Oh, wow. Only 3%.

SPEAKER_00Just 3%. Historically, I mean this program averaged about 9% growth every single year. So the days of explosive across the board enrollment growth are definitively behind us.

SPEAKER_01Aaron Powell So the pie is barely getting bigger. But the twist here is uh where that remaining 3% growth is actually coming from.

SPEAKER_00Aaron Powell Right. Because it's not evenly distributed.

SPEAKER_01Aaron Ross Powell Exactly. It is almost entirely concentrated in one specific area. Special needs plans or SPs. I was reading this and I kept thinking about it like a really popular restaurant.

SPEAKER_00Aaron Powell Okay, I like that. How so?

SPEAKER_01Well, imagine a wildly successful burger join. For a decade, they had a line around the block for their general menu. Everyone just wanted the standard burger and fries.

SPEAKER_00Aaron Powell Right, the basic, easy-to-understand package.

SPEAKER_01Exactly. But now the general menu isn't drawing new crowds anymore. The neighborhood is full, you know, everyone who wants a burger already has one. The only people keeping the business growing, the only ones forming a new line at the door, are the customers ordering from a highly specialized, highly complex dietary menu.

SPEAKER_00Aaron Powell That is a perfect way to look at it. Because what's fascinating here is the underlying demographic reality driving that analogy. Special needs clans are now 23% of the entire Medicare Advantage market.

SPEAKER_01Almost a quarter of the market.

SPEAKER_00Exactly. And if you go back to 2018, they were only 13%. According to the KFF report, SNPs accounted for a staggering 83% of total Medicare Advantage enrollment growth over the past year. Trevor Burrus, Jr.

SPEAKER_01Wait, 83% of all new growth came from just those specialized plans?

SPEAKER_00Yes. That is nearly 900,000 new enrollees in just these specialized plans. Meanwhile, the general plan enrollment had its absolute slowest growth rate since 2007.

SPEAKER_01Aaron Powell Okay, so what exactly is the mechanism here? Like why is the specialized menu suddenly the only thing keeping the lights on for these insurers?

SPEAKER_00Aaron Powell It represents a fundamental structural shift toward what we call the dual eligible and chronic condition populations.

SPEAKER_01Okay, define dual eligible for us.

SPEAKER_00Aaron Powell Sure. A dual eligible beneficiary is someone who qualifies for Medicare because of their age or a disability, but they also qualify for Medicaid because of their low income.

SPEAKER_01Oh, okay. So they have both.

SPEAKER_00Aaron Ross Powell Right. And these are incredibly complex high-need patient populations. The general market, you know, the relatively healthy 65-year-olds aging into the system who just want a standard plan with a free gym membership, that market has hit a saturation point.

SPEAKER_01Aaron Powell Like the neighborhood where everyone already has their burger.

SPEAKER_00Exactly. Most of the people who want a standard Medicare Advantage plan already have one. So the growth engine has shifted entirely to populations that require highly coordinated care for severe chronic conditions. I see. Insurers are realizing that if they want to capture new members, they actually have to build the infrastructure to manage very sick, very low-income populations.

SPEAKER_01Aaron Powell And because the general market is completely tapped out, the insurance carriers who couldn't pivot their menus fast enough are just getting absolutely crushed.

SPEAKER_00Aaron Powell Oh, crushed is the right word.

SPEAKER_01Aaron Powell Which explains this massive corporate bloodbath we are seeing in the KFF numbers. Let's look at the carriers themselves, because the shift to these special needs plans caused an absolute earthquake among the giant insurance corporations.

SPEAKER_00Aaron Powell It really did. I mean the KFF numbers show a brutal divergence in the market right now.

SPEAKER_01Aaron Powell Yeah. So on one side you have Humana, who gained, what, 1.2 million members across all their plan types?

SPEAKER_00Yep, 1.2 million. And Kaiser Permanente added about 64,000. Aaron Powell Right.

SPEAKER_01But then you look at the other side of the ledger, and the losses are just historic. United Health Group bled 530,000 enrollees. Eleven Health lost 368,000 members. CVS Health lost 29,000.

SPEAKER_00Trevor Burrus And while those massive publicly traded giants were bleeding hundreds of thousands of members, 150 smaller regional insurers collectively gained 734,000 members.

SPEAKER_01Aaron Powell Okay, wait. I have to push back on this premise a little bit. Sure. I understand that the general market is slowing down, but United Healthcare and Elephants are absolute behemoths. Aaron Powell. I mean, they have practically infinite financial resources, massive marketing budgets, endless data. Why couldn't a giant like United just, I don't know, buy their way into the SNP market or at least absorb the losses by heavily subsidizing their general plans? How does a dominant corporation just lose half a million people in a single year to a bunch of smaller regional players?

SPEAKER_00Aaron Powell It is a great question. And it really speaks to a misunderstanding of how risk pools actually work in this space.

SPEAKER_01Aaron Powell Okay, tell me more.

SPEAKER_00Aaron Powell You cannot just market your way out of a fundamentally broken math equation. If we connect this to the broader picture, the Milliman actuarial data perfectly illustrates why those giants bled members. Trevor Burrus, Jr.

SPEAKER_01So it comes down to the actuaries.

SPEAKER_00Always. In Medicare Advantage, beneficiaries are incredibly sensitive to the actual value a plan delivers. I'm talking about the tangible benefits, the out-of-pocket costs, the networks. The Milliman data reveals a direct, undeniable correlation between benefit competitiveness and enrollment outcomes.

SPEAKER_01Aaron Powell Meaning the consumer is actually paying very close attention to the math. It's not just about flashy TV commercials.

SPEAKER_00Exactly. When carriers like United, CVS, and Elevents looked at their internal data, they realized their risk pools were getting way too expensive to maintain. Trevor Burrus, Jr.

SPEAKER_01Because healthcare costs in general are just skyrocketing.

SPEAKER_00Aaron Powell Right. Healthcare costs were rising, but the government payments they received per member weren't keeping up. So to protect their corporate margins, they had to actively reduce the value-added benefits they offered. They shrank the networks, they cut the perks, and the moment they did that, the market punished them for it.

SPEAKER_01Wow. Trevor Burrus, Jr. Beneficiaries simply walked away and found regional players who were still offering better value. Meanwhile, Humana went the other direction. They managed their risk pools differently, their value-added benefits actually improved, and as a result, they saw a 22% spike in enrollment.

SPEAKER_00So Humana essentially built a better mousetrap while the other giants were actively dismantling theirs just to save money.

SPEAKER_01Aaron Powell That's a great way to put it.

SPEAKER_00But you know, when national carriers restructure their entire business model and suddenly pull back, the patients fall directly into the void. Aaron Powell They do. And that brings us to the most alarming part of these reports the displacement crisis. Here's where it gets really interesting.

SPEAKER_01Aaron Powell Right. When we talk about corporations protecting their margins, we have to talk about what happens to the human beings on the other side of that spreadsheet.

SPEAKER_00Exactly.

SPEAKER_01We have data from Johns Hopkins and Reuters showing that a staggering 2.9 million people were forced to find new coverage for 2026 because their plans were simply terminated. Aaron Powell.

SPEAKER_00Yes. That is roughly one in ten of all Medicare Advantaged participants. Ten percent of the entire market just entirely displaced.

SPEAKER_01Aaron Powell One in ten. And when you dig into the demographics of who got displaced, it is not evenly distributed at all. Aaron Ross Powell Not even close. Aaron Ross Powell The geographic divide is jaw-dropping. Rural enrollees were hit twice as hard as urban ones. The state level data is what really caught my eye. We mentioned Vermont earlier. Right. Vermont. Vermont saw 92% of its Medicare Advantage enrollees displaced. 92%.

SPEAKER_00That's unbelievable.

SPEAKER_01Trevor Burrus And other predominantly rural states like Wyoming, North Dakota, South Dakota, Maryland, and New Hampshire, they were also heavily affected. And it's not just where people live, it's the types of plans they lost.

SPEAKER_00Exactly.

SPEAKER_01PPO plans, which you know, the ones that give you more freedom to see out-of-network doctors, they saw a 12% decline compared to just an 8% drop for the more restrictive HMOs.

SPEAKER_00Aaron Ross Powell Right. And this raises an important question about the underlying architecture and math of the Medicare Advantage program itself. Hannah James, a policy researcher at the RAN Corporation, brought this up in an accompanying editorial to the Johns Hopkins study.

SPEAKER_01What'd she say?

SPEAKER_00She points out that the current structure of Medicare Advantage compensates insurers based on pre-agreed terms and benchmarks set by the government.

SPEAKER_01Right. So the government says we will give you X amount of dollars to manage this specific patient for the year.

SPEAKER_00Precisely. But here is how that mechanism completely breaks down in rural areas. When you combine those fixed government financial terms with skyrocketing fluctuating health care costs, it absolutely incentivizes insurers to target more profitable patient populations in urban centers.

SPEAKER_01Because providing broad PPO networks in sprawling, sparsely populated rural areas is just incredibly expensive.

SPEAKER_00It is. Exactly. But in rural Wyoming or South Dakota, there is no hospital across the street. Right. There might be only one cardiology clinic within 100 miles. That clinic holds literally all the leverage. They can demand astronomically high reimbursement rates, and the insurer has to pay it if they want to offer a network there.

SPEAKER_01Oh, I see.

SPEAKER_00When you combine those high provider costs with a PPO plan, which legally allows the patient to travel out of network to see specialists anyway, the math for the insurer simply implodes.

SPEAKER_01Aaron Powell Because the government is giving them a fixed dollar amount, but the rural hospital is charging basically whatever it wants. So the insurers are just making coal calculated business decisions to exit those unprofitable counties entirely. Are they just cherry-picking the profitable zip codes?

SPEAKER_00That's exactly what Hannah James notes. Those corporate margin protection decisions sacrifice continuity of care for the beneficiary.

SPEAKER_01It's devastating.

SPEAKER_00For someone in rural North Dakota, a PPO isn't a luxury. It's an absolute necessity because their nearest specialist might be two hours away and entirely out of a standard HMO network. When that plan vanishes, that patient's entire healthcare ecosystem is just completely disrupted.

SPEAKER_01Wow. So that is the reality for the 2.9 million people whose healthcare was completely upended.

SPEAKER_00Yeah.

SPEAKER_01But, you know, what about the other 90%? The people who opened their mail breathed a huge sigh of relief and realized they actually got to keep their plan.

SPEAKER_00Well, they aren't off the hook.

SPEAKER_01Right. According to the Milliman Actuarial Analysis, they didn't escape the chaos at all. They're just paying the price in an entirely different way. Let's talk about the shrinkflation of Medicare advantage benefits.

SPEAKER_00Shrinkflation really is the perfect term for the mechanism the actuaries are tracking right now.

SPEAKER_01It's exactly like what you see at the grocery store. You buy your favorite box of cereal. The cardboard box looks exactly the same size on the shelf. The branding is identical, the price is the same, but you open it up, and the bag inside is only half full.

SPEAKER_00Yep.

SPEAKER_01The insurance companies are keeping the brand names of their general plans the same, but they are quietly putting way less actual healthcare coverage inside the box.

SPEAKER_00Exactly. Let's look at the millimen numbers on that.

SPEAKER_01Yeah, Liam out.

SPEAKER_00The total value added fell by $17 per member per month, which, by the way, follows a $12 drop from the year before. Ouch. And the non-Medicare supplemental benefits, you know, the dental, the vision, the over-the-counter pharmacy cars that were so popular, those fell by $7 per member per month.

SPEAKER_01Aaron Powell And I think we should clarify the mechanism of what per member per month or PMPM actually means. Because I mean $17 doesn't sound like a crisis to the average person. Trevor Burrus, Jr.

SPEAKER_00doesn't sound like a lot, right? Right.

SPEAKER_01I mean, it sounds like a decent lunch. Why is that specific metric so devastating? Aaron Powell Okay.

SPEAKER_00Think of an insurance risk pool like a giant town reservoir. Everyone in the town pays into it, and when someone's house catches fire, the town uses the water to put it out. When an actuary says benefits fell by $17 PMPM, they aren't talking about one person's wallet. Right. They are talking about taking $17 out of the reservoir for every single person every single month. Oh wow. If an insurer has $5 million members, a $17 PMPM reduction means they are draining over a billion dollars a year out of the benefit pool.

SPEAKER_01A billion dollars.

SPEAKER_00Yes. It is a massive aggressive reduction in actual care being delivered to the consumer. The consumer doesn't see a $17 line item deduction. They see that their entire dental allowance was gutted or their transportation benefit to the doctor was completely eliminated.

SPEAKER_01Aaron Powell And the shrinkflation goes even deeper than just losing the free gym membership. The Milliman report highlights the death of the zero premium plan. Two hundred and thirty-one zero premium plans were completely wiped out from the market for 2026.

SPEAKER_00Aaron Powell Which is a historic reversal. For years the zero premium plan was the ultimate growth magnet.

SPEAKER_01Right, everyone wanted the free plan.

SPEAKER_00Exactly. Insurers heavily subsidized those plans, essentially using them as loss leaders to capture massive market share, assuming the government benchmarks would eventually make them profitable down the line.

SPEAKER_01But now that the math has inverted, those subsidies are just gone.

SPEAKER_00Completely gone.

SPEAKER_01But here is the most shocking statistic of all to me regarding this shrinkflation. The Part D prescription drug deductibles.

SPEAKER_00Oh yeah. This is huge.

SPEAKER_01According to Milliman, the average Part D deductible jumped from about $230 in 2025 to $375 in 2026.

SPEAKER_00And just look at the historical context on that.

SPEAKER_01Right. If you look back just two years to 2024, only 23% of members had a Part D deductible at all. Most people paid absolutely nothing out of pocket before their drug coverage kicked in. Now in 2026, 83% of members have a deductible.

SPEAKER_00That is a staggering shift in risk in just 24 months, and it perfectly validates your shrinkflation analogy from earlier. The massive carrier exits we discussed in the rural markets and this benefit erosion for the people who got to keep their plans, they are literally two sides of the exact same coin.

SPEAKER_01Aaron Powell Because the insurers are trying to balance the same broken equation.

SPEAKER_00Exactly. The insurance carriers are under immense financial pressure. If they couldn't make the math work in a rural county, they pulled out completely. If they stayed in a county, they made the math work by shifting the financial burden quietly onto the consumer through these $375 hurdles.

SPEAKER_01Okay. So we have covered a massive amount of ground today. We've gone through the macro level data, the corporate bloodbath, the rural provider monopolies, and the actuarial math of a billion-dollar reservoir drain. But let's unify this and translate it into the ground game.

SPEAKER_00Aaron Powell Always the most important part.

SPEAKER_01Right. So what does this all mean? If you are listening to this, whether you're an independent agent trying to salvage a panic client's coverage, or you're just a son or daughter looking at your parents' new $375 deductible, the strategy has to change entirely. It moves from auto-renew to gap filling. What is the actionable advice here?

SPEAKER_00The primary takeaway is that the days of passively auto-renewing a Medicare Advantage plan without reading the fine print are completely over.

SPEAKER_01Aaron Powell The box has less cereal in it.

SPEAKER_00Exactly. And you have to know exactly what is missing. If you are a beneficiary, you might be getting a premium bill for a plan that has been free for five years. Or you might walk into a pharmacy to get your routine daily medication and suddenly hit a $375 out-of-pocket wall that simply wasn't there last year. Right. You have to actively audit your coverage. Now, if you are an insurance agent or a broker, this data points to a once-in-a-decade opportunity because chaos creates a massive need for guidance.

SPEAKER_01Well, yeah, you have 2.7 million displaced non-SNP members who are actively shopping right now because their old plan literally ceased to exist. Trevor Burrus, Jr.

SPEAKER_00Precisely. In heavily affected rural states, the market is wide open. These aren't cold calls. These are people who urgently need someone to help them navigate a system that just abandoned them. But even for the clients who kept their plans, the shrinkflation aspect points to a vital cross-cell strategy. Because the primary Medicare Advantage plans are shrinking their core benefits and increasing out-of-pocket maximums. There is a massive opening to offer supplemental coverage to patch those holes.

SPEAKER_01What does that look like in practice? Because I mean, if an MA plan strips away its robust dental coverage, the beneficiary still has teeth. They still need that care.

SPEAKER_00Exactly. Agers should be looking at standalone dental vision and especially hospital indemnity plans.

SPEAKER_01Oh, wait, can you explain the mechanism of a hospital indemnity plan for someone who might not be familiar with the term?

SPEAKER_00Of course. A hospital indemnity plan is a supplemental policy that pays a fixed cash amount directly to the patient if they are hospitalized.

SPEAKER_01Ah, so it goes to the patient, not the hospital. Trevor Burrus, Jr. Right.

SPEAKER_00It doesn't pay the hospital at all, it pays the patient. So if a client's Medicare Advantage plan suddenly introduces, say, a $400 daily copay for a hospital stay because of shrinkflation, a hospital indemnity plan can provide the cash to cover that exact out-of-pocket cost.

SPEAKER_01That is incredibly smart.

SPEAKER_00The agent who can explain why the primary plan changed and then offer a tailored supplemental product like an indemnity plan to bridge that specific financial gap, they transition from being just a salesperson to being an essential trusted advisor.

SPEAKER_01Aaron Powell That makes total sense. You identify the specific gap the insurer created in the reservoir, and you provide the exact patch to fix it.

SPEAKER_00Exactly.

SPEAKER_01What an incredible journey we've taken through this data today. We started by looking at the explosive, almost exclusive rise of special needs plans, which are basically the only thing keeping the overall market afloat right now.

SPEAKER_00Yep.

SPEAKER_01We tracked the corporate reshuffling that saw massive giants like United Bleed members because their risk pools got too expensive, while regional players swooped in. We unpacked the devastating rural displacement crisis driven by the math of fixed benchmarks and provider monopolies. And finally, we face the reality of benefit shriekflation, where the death of the zero premium plan means millions are suddenly paying $375 out of pocket just to start their prescription coverage.

SPEAKER_00And you know, when you synthesize all of those distinct data points, the KFF enrollment stagnation, the Johns Hopkins displacement study, the Millenman extuarial analysis, it leaves us with a truly profound, almost existential question about the future of American healthcare.

SPEAKER_01Oh, what's that?

SPEAKER_00We are seeing general enrollment stagnate, broad benefits erode, and hyper-specialized special needs plans drive all the growth. If the private Medicare advantage market becomes entirely tailored and profitable only for the very sick and the very poor, does traditional government-run Medicare suddenly become the default plan for the relatively healthy?

SPEAKER_01Wow. I hadn't even thought of that.

SPEAKER_00And if that happens, if healthy people flood back into traditional Medicare because the private market stripped away all their perks, can the federal government actually afford that demographic flip without the private sector there to absorb the risk? We could be looking at an absolute inversion of the Medicare system as we know it. Trevor Burrus, Jr.

SPEAKER_01That is an incredibly provocative thought to end on. If the general menu isn't profitable anymore, the private restaurant stops serving it, and everyone goes back to eating at the government cafeteria. Thank you so much for joining us on this deep dive. Navigating this landscape requires absolute vigilance. So keep asking the hard questions, keep reading the fine print, and never assume the box on the shelf has the same amount of coverage inside as it did last year. Until next time.