The Insurance Producers Guild

The Insurance Producers Guild is a strategic briefing for insurance professionals, focused on Medicare, ACA, life insurance, and the evolving insurance landscape. Each episode distills complex industry changes into clear, practical intelligence.

The Insurance Producers Guild

EP7 The AI Frontier: Future Proofing Your Agency

Use Left/Right to seek, Home/End to jump to start or end. Hold shift to jump forward or backward.

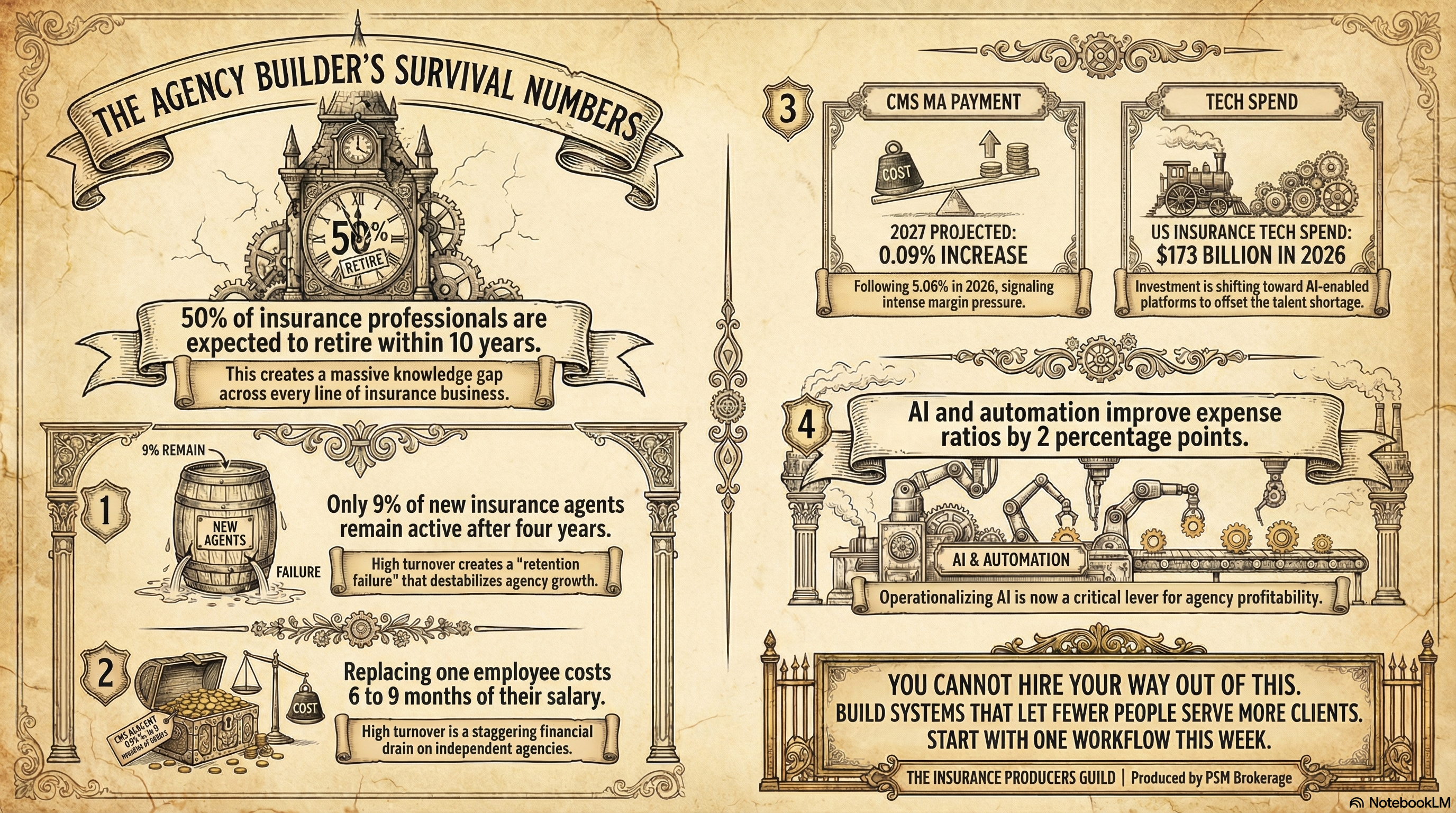

The insurance industry is entering a major workforce transition. According to data from the National Association of Mutual Insurance Companies (NAMIC), nearly half of all insurance professionals are expected to retire within the next decade. At the same time, retention challenges remain steep, with LIMRA reporting that only 9% of new agents are still active after four years.

Layer onto that a shifting economic landscape: the Centers for Medicare & Medicaid Services (CMS) CY 2027 Advance Notice proposes just a 0.09% Medicare Advantage payment increase—down significantly from 5.06% in 2026—putting pressure on plan margins, benefits, and service areas.

In this episode of The Insurance Producers Guild, we break down what these converging forces mean for independent agents—and why the solution isn’t hiring more, but building smarter.

With U.S. insurance technology spending reaching $173 billion in 2026 (according to Forrester), AI and automation are no longer optional. From automating client follow-ups to streamlining renewals and reducing administrative workload, agents now have the tools to scale efficiently—even with a shrinking workforce.

We also explore a powerful client retention strategy built around response speed, and why multi-line diversification is becoming critical in a tighter 2027 rate environment.

This episode is focused on helping agents future-proof their agencies—by combining operational efficiency, smarter systems, and strategic positioning.

🔑 Key Topics Covered

- Insurance workforce crisis and projected retirement wave

- Agent retention challenges and long-term sustainability concerns

- CMS CY 2027 Advance Notice and near-flat Medicare Advantage payment growth

- Impact of margin pressure on plan benefits and service areas

- Rise of AI and automation in insurance operations

- Identifying high-impact automation opportunities within an agency

- Client retention strategy centered on response speed

- Importance of multi-line diversification in a changing rate environment

- How to scale an agency without relying on increased hiring

🎯 What This Means for Agents

- Workforce shortages will increase competition for experienced agents and strain traditional growth models

- Automation is no longer optional—it’s essential for scaling with fewer resources

- Agencies that invest in technology can handle larger books of business more efficiently

- Faster response times can become a key competitive advantage in client retention

- Medicare Advantage margin pressure may lead to reduced benefits, requiring stronger value-based conversations

- Diversifying product lines can help stabilize revenue in uncertain rate environments

- Agents who build systems—not just teams—will be better positioned to survive and grow

Infographic: https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/IPG_EP7_Infographic.png

{kind=link}

Slides: https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/IPG_EP7_Slides.pdf

🔗 Sources

- National Association of Mutual Insurance Companies workforce data

- LIMRA 2025 agent retention report (via InsuranceNewsNet)

- Forrester U.S. insurance tech spending forecast (February 2026)

- Insurance Business Magazine turnover data (2024)

- Forbes turnover cost analysis (2024)

- Centers for Medicare&

The Insurance Producers Guild Podcast delivers intelligence for insurance agents looking to stay ahead of industry trends.

Follow the show and connect with PSM Brokerage to access tools, training, and support designed to help you grow your business.

Learn more: https://www.psmbrokerage.com

You know, you are probably staring at the ceiling at two in the morning, completely stressed out.

SPEAKER_01Oh, absolutely. That is a very real thing.

SPEAKER_02Right. You are drowning in compliance paperwork, your inbox is an absolute disaster. And well, you are wondering why you just cannot seem to find good people to hire anymore.

SPEAKER_01Yeah, it is a terrible feeling.

SPEAKER_02It really is. But what if I told you that you do not need better hires? You need better systems.

SPEAKER_00Exactly.

SPEAKER_02Today we are going to look into the data and show you why trying to hire your way out of this current market is frankly a complete trap.

SPEAKER_01It's it a trap.

SPEAKER_02I am going to map out the historical patterns of this market because you know I have been through this before. And my partner here is going to give you the exact scripts and monetization tactics to use in the field this week.

SPEAKER_01Aaron Powell That is right. And I want to tell you directly that this stress you are feeling, it is not a personal failure.

SPEAKER_02No, not at all.

SPEAKER_01It is not a flaw in how you run your agency. What you are feeling right now is a massive industry-wide reality. You know, you are feeling the weight of an entire market shifting beneath your feet.

SPEAKER_02Aaron Powell Yeah, the ground is moving.

SPEAKER_01Aaron Powell But the good news is that we are going to look at the math today and we are going to turn that data into revenue.

SPEAKER_02Aaron Powell Let's start with the math then. Because the numbers are, well, they are frankly staggering.

SPEAKER_00They really are.

SPEAKER_02The latest demographic data from NAMIC, the National Association of Mutual Insurance Companies, reveals that 50% of insurance professionals will retire within the next 10 years.

SPEAKER_00Wow. 50%.

SPEAKER_02Think about that for a second. Half of the institutional knowledge in our industry is literally walking out the door. Just gone. Right. Now, I have been through this before. Every decade or so, the industry loses a generation. I saw it in the late 90s. And uh I saw it again around 2010 when healthcare regulations totally changed the landscape.

SPEAKER_01Aaron Powell And what actually happened to the agencies during those shifts?

SPEAKER_02Aaron Ross Powell Well, the agents who survived those shifts built systems. The ones who failed, they built themselves into a corner by relying entirely on individual knowledge and sheer manpower.

SPEAKER_01Aaron Powell Oh, yeah. I know exactly what you mean.

SPEAKER_02Aaron Powell You know the type. It is the senior agent who knows exactly which carrier underwrites diabetes favorably without looking at a manual.

SPEAKER_01Trevor Burrus Right. It is all in their head.

SPEAKER_02Exactly. When that agent retires, that knowledge vanishes unless it is codified into a system.

SPEAKER_01Aaron Powell And you just cannot replace that manpower anymore. No. I mean the retention numbers are brutal right now.

SPEAKER_02Aaron Ross Powell They really are.

SPEAKER_01Aaron Ross Powell If we look at the latest retention studies from L I M R A, you know, the premier research group for our field, the four-year agent retention rate is a devastating nine percent.

SPEAKER_02Aaron Powell Wait, nine percent.

SPEAKER_01Nine percent. That means out of every 100 agents who get licensed and enter the business, 91 of them are gone within four years.

SPEAKER_02Aaron Powell That is just unbelievable. You know, relying on manual hiring right now is like it is like running a restaurant where the kitchen staff quits after the appetizer.

SPEAKER_00That is a great way to put it.

SPEAKER_02You spend all your money training them to chop onions, and by the time the main course arrives, you are back on the grill yourself. You are pouring energy, time, and capital into an absolute void. So I really have to push back on agency owners who tell me they just need to run more ads on job boards. Because you cannot outhire a 91% turnover rate.

SPEAKER_01No, you cannot. Let's talk about the actual dollar amount of that turnover too, because the financial reality is severe. Let's hear it. We reviewed a recent Forbes analysis on the cost of turnover. And it shows that replacing an employee costs, well, it costs six to nine months of their salary.

SPEAKER_02Wow.

SPEAKER_01Let's put that into real agency terms. Yeah. If you hire a producer at $60,000 a year and they walk out the door, that is a $30,000 to $45,000 loss every single time they quit.

SPEAKER_02Okay, hold on. $45,000 for a $60,000 employee. Yeah. I mean, agency owners listening right now are probably rolling their eyes at that. Where is Forbes getting that math? Because to a local independent agent, you know, that sounds completely inflated.

SPEAKER_01Oh, I know. It sounds inflated until you actually do the accounting.

SPEAKER_02Okay, walk me through it.

SPEAKER_01We are not just talking about the physical paycheck. Yeah. We are talking about all the hidden costs. Think about the 30 hours of your own management time spent interviewing.

SPEAKER_02Right. Your time is money.

SPEAKER_01Exactly. Think about the background checks, the licensing fees, the EO insurance. Then consider the fact that for the first 90 days, they produce almost zero revenue while they learn the ropes.

SPEAKER_02That makes sense.

SPEAKER_01But the biggest hidden cost, the absolute biggest, is the leads they burn. Oh, yeah, the leads. If you feed a new agent 20 expensive high-intent leads and they fumble them because they are inexperienced, well, that is bottom line revenue evaporating.

SPEAKER_02It is painful to watch.

SPEAKER_01I remember running an agency early on where we lost three producers in one single quarter. We bled over a hundred grand and sunk training costs and lost production. You simply cannot sustain that model.

SPEAKER_02You absolutely cannot. And you know, this is exactly why PSM brokerage heavily emphasizes operational systems for its partners. Agencies must systematize to survive. 100%. You have to capture the knowledge of your best people and put it into a process that runs regardless of who is sitting in the chair.

SPEAKER_00Right.

SPEAKER_02Since trying to hire your way out of a 9% retention rate is mathematically impossible, you are left with only one alternative. You have to buy software that does not quit.

SPEAKER_01That is the truth. That brings us to the technology that actually buys back an agent's time.

SPEAKER_02The shift happening right now is, well, it is unprecedented. According to the Forrester data, insurance tech spending hit $173 billion in 2026.

SPEAKER_01Hold on. $173 billion?

SPEAKER_02Yeah, with a B.

SPEAKER_01That number is so large, it almost loses its meaning for a local agency owner. Like how much of that is actually trickling down to the tools we use on Main Street?

SPEAKER_02That is the best part, honestly. It is not just enterprise giants hoarding this tech anymore. That massive injection of capital means enterprise-level artificial intelligence is moving from simple pilots down to ground level operations, operations that independent agents can actually use.

SPEAKER_00Okay, that is huge.

SPEAKER_02We are seeing specific tool applications that directly impact the everyday agent. For example, Easy Links is embedding artificial intelligence to cut manual task time in half.

SPEAKER_01But how exactly does it cut the time in half, though? What is the actual mechanism there?

SPEAKER_02Okay, think about a client census or a medication list. Instead of your staff staring at a PDF and manually typing names, dates of birth, and prescriptions into five different fields across multiple carrier portals.

SPEAKER_00Which is the worst part of the job.

SPEAKER_02Exactly. The system uses optical character recognition, it reads the document, understands the context, and auto-populates your CRM in about three seconds.

SPEAKER_01That is incredible.

SPEAKER_02It eliminates the redundant data entry that makes your staff want to quit in the first place. And uh we are not talking about multi-million dollar software packages here. Right. Modern CRM platforms only cost $15 to $50 a month. This makes high-level automation accessible to literally any independent agent operating today.

SPEAKER_01So the cost barrier is totally gone.

SPEAKER_02Completely.

SPEAKER_01Now it is just a matter of adoption. But how does an agent actually monetize that save time? Tell them. Stop. Let me give you the script. This is the two-minute retention rule, and it works every single time in the field. I love this one. When a client calls with a question, the agent who answers in two minutes keeps the client. The agent who takes two days loses them. It is that simple. Systems give you the two-minute answer.

SPEAKER_02Walk us through what that actually looks like when the phone rings.

SPEAKER_01Okay. Let's say Mrs. Smith calls about an over-the-counter benefit allowance or a specific network question.

SPEAKER_02Pretty common call.

SPEAKER_01Very common. If you are running an outdated agency, you have to tell her, let me look into that and call you back. Then you spend 20 minutes digging through carrier portals and well, maybe you call her back tomorrow.

SPEAKER_02And you look unorganized.

SPEAKER_01You look completely disorganized. But if your CRM pulls up her entire profile instantly with automated summaries, the second the phone rings, you handle it right then on the call. You say, Yes, Mrs. Smith, you have a $50 quarterly allowance and you can use it at the pharmacy down the street. Boom. You look like an absolute genius, and she never, ever leaves you for another broker.

SPEAKER_02That is exactly how you have to look at it. The actionable advice here is that the technology is not here to replace the agent. It is here to handle the operational weight.

SPEAKER_00Exactly.

SPEAKER_02It takes the heavy lifting off your desk so you can focus entirely on client relationships, prospecting, and enrollment conversations. You should be spending your time talking to people, not fighting with spud sheets.

SPEAKER_01Spot on, this ties right into how PSM brokerage operates with its marketing hub, actually.

SPEAKER_02Oh yeah. That is a great example.

SPEAKER_01They handle the co-branded materials for you. That allows agents to spend their time actually selling and having those enrollment conversations rather than wasting three hours trying to design a flyer on their computer. Trevor Burrus, Jr.

SPEAKER_02Because nobody got into this business to be a graphic designer.

SPEAKER_01Exactly. You systematize the marketing so you can execute the close.

SPEAKER_02And we really need to execute the close right now because the market is not waiting for anyone to catch up.

SPEAKER_00No, it is not.

SPEAKER_02Efficiency is not just a luxury anymore. It is an absolute emergency because of what CMS, the Centers for Medicare and Medicaid Services, is doing for 2027.

SPEAKER_01Aaron Powell Yeah, the margins are getting incredibly tight.

SPEAKER_02Let's break down the math on the 2027 rate squeeze.

SPEAKER_00Let's do it.

SPEAKER_02The CMS 2027 advance notice shows a microscopic 0.09% payment increase for the upcoming year. Wow. Compare that to the 5.06% increase that was finalized for 2026. That is a massive drop in funding growth. The government is adjusting their risk adjustment models and uh dealing with shifting utilization patterns.

SPEAKER_00Right.

SPEAKER_02Now the final rate announcement is due on April 6th, so we will see where it officially lands. But the writing is on the wall.

SPEAKER_01So what is the practical effect of that microscopic increase in the field? What does the agent actually experience?

SPEAKER_02Yeah. Well, the practical effect is that carriers have to make hard business decisions to keep the plans viable. And I want to be perfectly clear about this. This is absolutely not a criticism of our carrier partners.

SPEAKER_00No, of course not.

SPEAKER_02They are doing exactly what they have to do to keep the plans solvent in a tight regulatory environment.

SPEAKER_01They have to make the math work.

SPEAKER_02Exactly. But for the agent, you need to expect more plan exits, benefit cuts, and service area reductions. We are going to see disruption in the market, but you know, I view this explicitly as a massive opportunity.

SPEAKER_00I love that. Disruption is just another word for circulating leads.

SPEAKER_02Aaron Powell That is exactly what it is. Movement means you have the chance to capture orphaned clients who are confused and need guidance. When a plan exits a county, those seniors do not just disappear.

SPEAKER_01No, they still need coverage.

SPEAKER_02They need an agent to help them transition to a new plan.

SPEAKER_01That is the closer mentality right there. And there is a major silver lining for sales in the CMS final rule that agents really need to understand.

SPEAKER_02What is that?

SPEAKER_01CMS has been cracking down on confusing marketing, but they did not prohibit marketing the actual dollar value of supplemental benefits.

SPEAKER_02Oh, that is huge.

SPEAKER_01It is. Agents can still confidently quote specific benefit amounts when talking to clients.

SPEAKER_02So how does an agent use that at the kitchen table?

SPEAKER_01Okay, when you are sitting across from a prospect, you do not talk in vague terms. You can still talk about the exact dollar allowance for dental, vision, or over-the-counter benefits.

SPEAKER_02Right. Be specific.

SPEAKER_01You say, Mr. Johnson, this specific plan gives you exactly $1,000 a year for comprehensive dental.

SPEAKER_02Nice.

SPEAKER_01Showing tangible, quantifiable value is what closes the deal.

SPEAKER_02Which is absolutely critical. But you know, if benefits are getting trimmed across the board because of the rate squeeze, how do you protect your agency from shrinking commissions?

SPEAKER_01You have to diversify. I am going to give you a harsh but necessary field reality regarding your book structure.

SPEAKER_02Play out on them.

SPEAKER_01If MA Medicare Advantage is 80% of your book and plans keep exiting your territory, you do not have a business. You have a lottery ticket. Ouch.

SPEAKER_02But true.

SPEAKER_01You are entirely dependent on regulatory forces that you simply cannot control.

SPEAKER_02I have seen this exact pattern destroy agencies. They ride a single hot product line, the regulatory environment changes, the funding dries up, and they lose half the revenue overnight.

SPEAKER_00Exactly.

SPEAKER_02So how do you fix that structurally?

SPEAKER_01You spread the risk. That is exactly why PSM Brokerage provides dedicated business coaching to help agents build multi-line books. You need to be writing across Medicare, life, annuities, ACA under 65 health plans, and ancillary products.

SPEAKER_02Okay, give me a specific cross-cell play for that. How do you introduce an ancillary product naturally without being pushy?

SPEAKER_01Stop. Let me give you the script. Here is what I would say word for word.

SPEAKER_02Go ahead.

SPEAKER_01When you secure that Medicare Advantage application, you pivot immediately. You say, Mr. Johnson, we have your health coverage locked in. But this plan does have a $300 daily copay for an inpatient hospital stay.

SPEAKER_02Right, acknowledging the gap.

SPEAKER_01Exactly. Then you say, Let me show you how a small hospital indemnity plan covers that exact gap, so you pay zero out of pocket if you are admitted.

SPEAKER_02It makes so much sense.

SPEAKER_01When you cross-sell a Medicare client, a hospital indemnity plan, or you know, set them up with a small final expense life policy, you are building a moat around your business. No single product line can sink your revenue if you are properly diversified.

SPEAKER_02That is brilliant. Okay, let's summarize the actions you need to take this week based on everything we just covered.

SPEAKER_01Let's run through it.

SPEAKER_02First, stop relying on manual hiring to fix your structural problems. You cannot beat a 91% turnover rate with more interviews.

SPEAKER_00No, you cannot.

SPEAKER_02You need to accept that the talent pool is shrinking and adjust your strategy. Second, adopt the CRM systems and automation tools that enable that two-minute response. Buy back your time so you can actually get back to selling.

SPEAKER_01Yes. Automate everything you can.

SPEAKER_02And third, review your book diversification before that April 6th CMS final rate announcement. Look at your revenue split and start cross-selling ancillary products immediately.

SPEAKER_01I want to leave you with a final scenario to ponder, actually. And this should really light a fire under your operations. What is the scenario? Look at the data we reviewed from JAMA, the Journal of the American Medical Association. Their research showed that 2.9 million MA beneficiaries were affected by planned terminations for 2026 alone.

SPEAKER_022.9 million, that is massive.

SPEAKER_01Now imagine what happens if 2027 brings severe provider network terminations that trigger a special enrollment period. Oh wow. CMS has already acknowledged broad stakeholder interest in that possibility. If a major disruption hits your specific territory and suddenly thousands of seniors are looking for a new plan mid-year, do you currently have the CRM infrastructure to capture those thousands of circulating leads?

SPEAKER_02That is the real question.

SPEAKER_01Or will your manual paper based processes simply collapse under the weight of the opportunity?

SPEAKER_02That is the question you need to answer this week. Build the systems now so you are ready when the market moves. That's this Friday's The Insurance Producers Guild. Stay tuned for the next episode. If you're not already with PSM Brokerage, this is the kind of actionable intelligence our agents get. Talk to us about contracting.