The Insurance Producers Guild

The Insurance Producers Guild is a strategic briefing for insurance professionals, focused on Medicare, ACA, life insurance, and the evolving insurance landscape. Each episode distills complex industry changes into clear, practical intelligence.

The Insurance Producers Guild

EP8 Why High Deductible G Plus Hospital Indemnity Wins

Use Left/Right to seek, Home/End to jump to start or end. Hold shift to jump forward or backward.

Most independent agents have focused on Medicare Advantage, but heading into 2026, the data suggests a shift. Rising out-of-pocket maximums, reduced plan availability, and over 90% persistency in Medicare Supplement blocks are pushing beneficiaries toward provider access and predictable costs over extra benefits.

In this episode, two veteran agents break down a strategy gaining traction: pairing High-Deductible Plan G with hospital indemnity. The combination lowers monthly premiums, saves clients hundreds annually, and significantly reduces financial exposure in hospitalization scenarios.

The episode also addresses the “90% problem”: Most Medicare Advantage enrollees lack guaranteed issue rights to move to Medigap after their initial window. With common conditions like hypertension and diabetes, many clients may become uninsurable before they ever consider switching, making early conversations critical.

For agents, the takeaway is clear: Proactive conversations today can protect both clients and long-term retention.

🔑 Key Topics Covered

- 2026 Medicare Advantage trends: rising MOOPs and declining plan counts

- Medicare Supplement persistency exceeding 90%

- Why beneficiaries are shifting toward predictable cost structures

- High-Deductible Plan G strategy explained

- Hospital indemnity stacking and real-world cost scenarios

- Premium comparison: HDG + indemnity vs. standard Plan G

- The “90% problem” and Medigap eligibility limitations

- Chronic condition trends impacting underwriting (hypertension & diabetes)

- Commission stability in ancillary vs. Med Supp compression

🎯 What This Means for Agents

- Market momentum may be shifting back toward Medicare Supplement strategies

- High-Deductible Plan G + indemnity offers a strong value alternative to standard Plan G

- Early client education is critical before underwriting becomes a barrier

- Medicare Advantage clients beyond 12–24 months may be at risk of losing flexibility

- Ancillary products like hospital indemnity can improve both client outcomes and agent revenue stability

📌 GO-DO

- Review your book of business and identify Medicare Advantage clients enrolled for 2+ years

- Select 5 clients and reach out this week

- Use this opening: “I want to make sure you know your options before anything changes with your plan. Can I spend 10 minutes walking you through a comparison?”

- If you need to add Medicare Supplement or hospital indemnity products to your portfolio, connect with your PSM representative (https://www.psmbrokerage.com/contact)

Infographic: https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/EP8_Infographic.png

{kind=link}

Slides: https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/EP_8_Slides.pdf

🔗 Sources

- KFF (Kaiser Family Foundation) Medicare Data

- NAIFA Industry Insights

The Insurance Producers Guild Podcast delivers intelligence for insurance agents looking to stay ahead of industry trends.

Follow the show and connect with PSM Brokerage to access tools, training, and support designed to help you grow your business.

Learn more: https://www.psmbrokerage.com

You walk the floor of any major insurance conference right now, and well, you hear the exact same thing. You talk to agents who primarily sell Medicare Advantage, and they will tell you straight to your face that Medigap is completely dead.

SPEAKER_00Oh, completely. They think the market has just permanently moved on.

SPEAKER_01Right. They think anyone still talking about supplements is just, you know, stuck in the past. But uh if you actually look at the raw numbers for 2026, we are staring at the biggest structural resurgence of Medicare supplements in a decade. Agents selling only advantage plans are about to get left entirely behind.

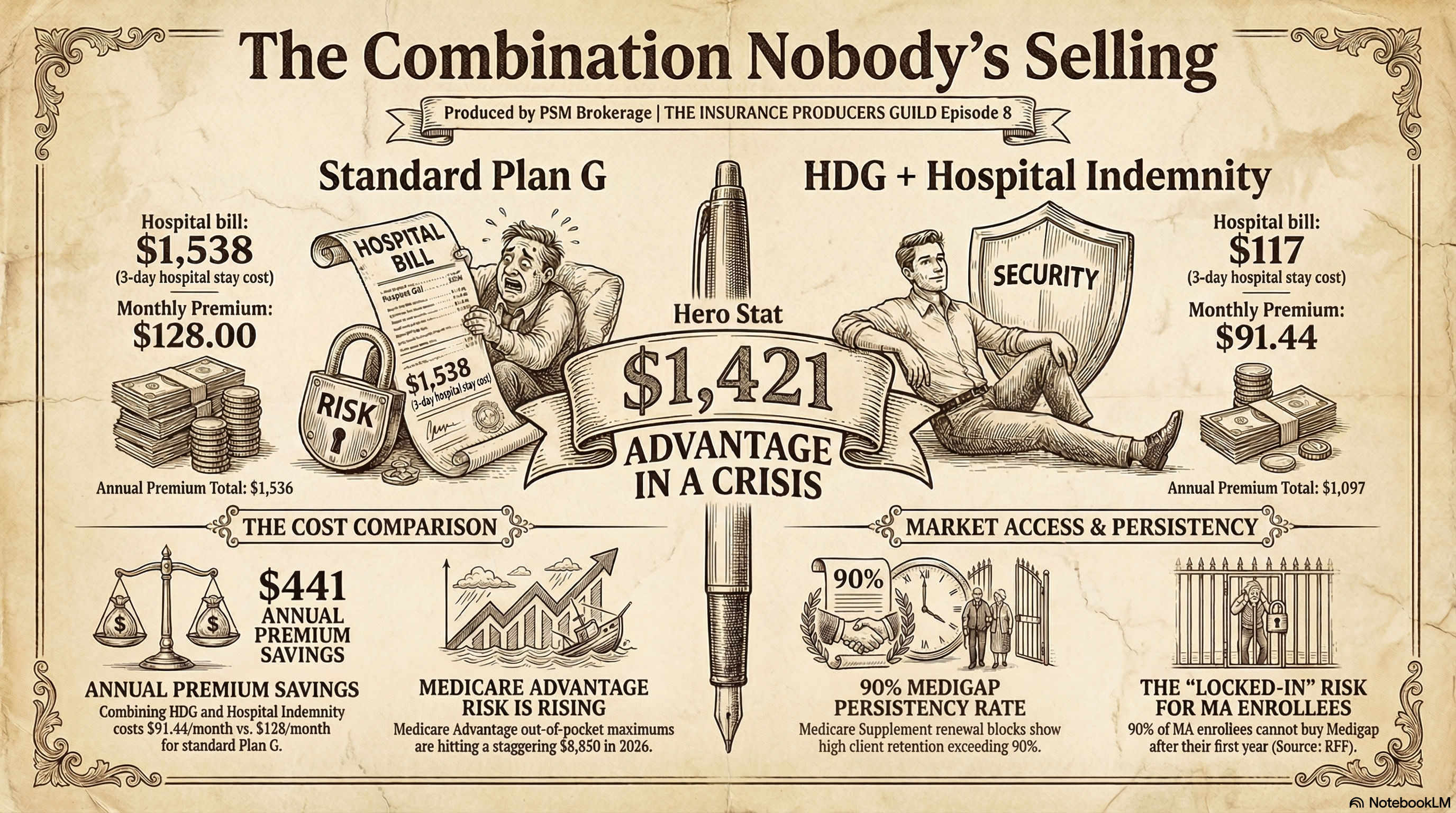

SPEAKER_00Yeah, they are completely missing the reality here. Let's just dissolve that advantage-only bias right now in the first 90 seconds. Look, Medicare Advantage out-of-pocket maximums are hitting $8,850. Wow. Meanwhile, Medigap persistency is sitting above 90%. And here is the real bombshell hook. The high deductible plan G plus hospital indemnity combination delivers better protection than standard plan G at $36 less per month. This is not nostalgia. It is math.

SPEAKER_01It really is. And you know, I have been through this before. I have seen this exact market cycle play out. When you have been in this business for over 25 years, well, you learn to spot the patterns. You definitely do. So we want to translate these shifting numbers into actionable plays for your book of business, your clients, and frankly, your commission statements, because right now we are seeing a measurable deterioration in Medicare Advantage Plan quality.

SPEAKER_00Absolutely. The financial reality for a lot of members is just becoming incredibly stark. The Centers for Medicare and Medicaid Services recently confirmed the first measurable reduction in advantage plan counts in several years.

SPEAKER_01Yeah, that was a big deal.

SPEAKER_00It was. We are seeing multiple national carriers actively consolidating their product portfolios. They are pulling out of counties where they are only marginally profitable. Right. And that leaves beneficiaries with fewer plan choices and much narrower provider networks.

SPEAKER_01Aaron Powell And we should be clear about that. You should never look at carrier consolidation as a negative thing. It is strictly an opportunity for you to review your contracts, check your rate competitiveness, and look for underwriting flexibility.

SPEAKER_00Aaron Powell That is a great point. There are regional and niche carriers gaining serious market share right now with competitive options.

SPEAKER_01Aaron Powell Yeah, exactly. But from the client's perspective, this consolidation is painful. I mean, the average medical maximum out-of-pocket limits increased from roughly $5,100 to $5,440.

SPEAKER_00And that is just the average, like we just said, those maximums are actually reaching $8,850 for in-network services alone in many markets. And uh that is strictly the medical side.

SPEAKER_01Right. Part D is a whole other story.

SPEAKER_00Yeah. Part D deductibles jump from roughly $230 up to $375 for most enrollees. Trevor Burrus, Jr.

SPEAKER_01Plus, we're seeing a huge drop in all those flashy extras that agents have loved selling for the past five years. Those non-Medicare supplemental benefits, well, they have dropped by $7 per member per month on average.

SPEAKER_00Which is huge.

SPEAKER_01It is. Zero premium plan availability actually declined by 9.5%. You can see the shift happening right at the kitchen table.

SPEAKER_00Aaron Powell It is a complete reversal in consumer sentiment. For a long time, you know, beneficiaries were drawn to the ancillary perks. They wanted the vision coverage, the over-the-counter grocery cards, the free gym memberships.

SPEAKER_01Oh, everybody wanted the free gym membership.

SPEAKER_00Right. But now consumer priorities are shifting back to the core elements of actual health care. They are realizing that a free gym membership is completely useless when they cannot afford the copay to see a specialist. Or worse, when their primary care doctor is suddenly dropped from the network.

SPEAKER_01Exactly. We have all had that frantic phone call where your client is standing at the doctor's front desk and they have just been told their network changed.

SPEAKER_00It is the worst call you can get.

SPEAKER_01It really is. That is the exact moment that $50 grocery card means absolutely nothing. I sold Medigap before MA existed. The clients who stayed with it never had a bad year.

SPEAKER_00That statement right there is backed up by the numbers. When we say persistency rates in MedSub blocks are exceeding 90%, what we mean is that these clients buy the policy and they stay put.

SPEAKER_01Because they have standardized, predictable coverage.

SPEAKER_00Exactly. They are not exposed to the annual volatility of advantage contracts, which constantly fluctuate based on carrier bid negotiations and federal star rating incentives. That stability translates to incredibly high member satisfaction.

SPEAKER_01And predictable commission income for your agency. The real question is how you monetize this consumer anxiety today. Clients are feeling the pinch of these rising out-of-pocket costs, and you need to step in and solve that problem.

SPEAKER_00Here's what I say: your MA plan's out-of-pocket max just went up again. Let me show you what a supplement would actually cost you versus what you're currently risking.

SPEAKER_01I love how direct that is. It addresses the immediate pain point without overcomplicating the pitch.

SPEAKER_00Keep it simple.

SPEAKER_01Right. And if you are working with PSM brokerage, you already know that agents have access to med subcontracting across top-tier carriers. You should absolutely talk to your PSM rep about your current portfolio to make sure you have the right products loaded up for these reviews.

SPEAKER_00That is a critical step. Yeah. Because the product landscape is shifting fast.

SPEAKER_01Okay. But I need to stop you there and push back on the strategy for a second. I love the idea of moving clients back to Medigap, but we both know the reality of the market right now.

SPEAKER_00The premiums.

SPEAKER_01Exactly. Standard plan G premiums are rising fast. We are seeing 20% increases in many states. A standard plan G for a 65-year-old is hitting $128 or more every single month.

SPEAKER_00Yeah, it is getting up there.

SPEAKER_01So how are you actually going to sell a $128 monthly premium to a fixed income senior who is used to a zero premium advantage plan? I mean, they're going to laugh you out of the house.

SPEAKER_00Well, that is exactly why you have to change the strategy. You cannot just blindly pitch a standard plan G anymore. The high deductible plan G plus a stacked hospital indemnity combination is the most compelling product development in the market right now.

SPEAKER_01Really?

SPEAKER_00Oh, absolutely. It completely solves that premium objection.

SPEAKER_01Explain that to me because the moment you pitch a high deductible anything, seniors immediately start to panic. The deductible for that plan is $2,870. You are hanging a nearly $3,000 risk right over their head.

SPEAKER_00Right, but you do not leave them exposed to that deductible. The high deductible plan G gives you the exact same comprehensive coverage as a standard plan G, once that $2,870 deductible is met. But the monthly premiums drop drastically.

SPEAKER_01So how do you protect them before they hit the deductible?

SPEAKER_00To protect them from the deductible itself, you fill that specific gap with a hospital indemnity plan. Think of it like buying a highly reliable car with a high deductible insurance policy from major recs, but then you buy a cheap separate roadside assistance plan to handle all the daily flat tires and tow trucks.

SPEAKER_01Okay, that makes sense. Walk me through the actual numbers on this. I want to see how this combination mathematically beats a standard plan G.

SPEAKER_00Let me break down the exact math of this stack. You start with a high deductible plan G. In competitive markets, you are looking at rates as low as $44.24 per month.

SPEAKER_01Wow, that is low.

SPEAKER_00Very low. Then you add the hospital indemnity base plan. A solid base plan that pays $300 a day for a six-day benefit period costs about $18.30 per month.

SPEAKER_01Okay.

SPEAKER_00Next, you stack on an outpatient surgery rider that pays a $500 lump sum. That is $13.26 per month.

SPEAKER_01So we are sitting around $75 a month so far. What else are you putting in this stack?

SPEAKER_00You add a cancer writer, which pays a $2,500 lump sum immediately upon diagnosis. That is just $4.47 per month.

SPEAKER_01Less than five bucks.

SPEAKER_00Exactly. Finally, you add a skilled nursing writer that pays $100 per day for up to 50 days. That writer costs $11.17 per month.

SPEAKER_01Let me make sure I have all these pieces. You have the high deductible plan, the hospital base, the surgery writer, the cancer writer, and the skilled nursing writer.

SPEAKER_00That is the complete stack.

SPEAKER_01So if you add all those premiums together, what is the total out-of-pocket for the client each month?

SPEAKER_00The total monthly cost for that package is $91.44. Now compare that to a standard plan G, which sits at $128.21 per month. By building this specific combination, you are saving the client $36.77 every single month.

SPEAKER_01That is huge for a fixed income.

SPEAKER_00It really is. That is $441 a year staying in their pocket, and they actually have more comprehensive coverage for hospitalization scenarios.

SPEAKER_01Let's test that out. I want to walk through a real-world claim scenario to prove that the math actually works when the client gets sick.

SPEAKER_00Let's do it.

SPEAKER_01Take a client who has a three-day hospital stay, followed by 28 days of skilled nursing rehab. If that client just bought a standard plan G, they are paying $1,538 annually just in premiums.

SPEAKER_00Exactly. But with the high deductible G plus hospital indemnity combo, their total out-of-pocket cost for that entire medical event drops to just $117.

SPEAKER_01Wait, how does it get that low? Break down the exact mechanics of that payout. When the client is actually dealing with the billing department, how does this function?

SPEAKER_00Well, the hospital indemnity policy steps in and pays out cash directly to the client. The money does not go to the doctor or the hospital, it goes straight into the client's bank account.

SPEAKER_01Oh, nice.

SPEAKER_00Right. So for the three-day hospital stay, the base plan pays $300 a day, which is $900. For the $28-day rehab, the skilled nursing writer pays $100 a day, which is $2,800. So the indemnity policy hands the client a total cash payout of $3,700.

SPEAKER_01And the client takes that $3,700 cash and uses it to completely wipe out the $2,870 deductible on the high deductible plan G.

SPEAKER_00Precisely. The cash payout largely offsets the deductible. And they even have some money left over for other expenses. The client is completely financially protected. They saved $441 in their monthly premiums throughout the year, and they are not stressed about a massive surprise bill arriving in the mail.

SPEAKER_01Agents who learn this math before everyone else does will have a real edge. This is a massive value add for the client.

SPEAKER_00Oh, absolutely.

SPEAKER_01And there's another layer to this that makes it a huge win for your agency's revenue. Hospital indemnity is a guaranteed issue for ages 60 to 79 using simplified underwriting.

SPEAKER_00Yes, that simplified underwriting is key. It is just a short list of serious conditions. Clients cannot be denied for high blood pressure. They cannot be denied for well-managed diabetes without serious complications.

SPEAKER_01It's way easier. And from a pure business perspective, the commission angle is rock solid. We are seeing Medicare Advantage and even standard med subcommissions getting squeezed in certain areas, but carrier commissions on hospital indemnity have remained completely stable.

SPEAKER_00They really have.

SPEAKER_01You earn more revenue per client while providing genuinely better value.

SPEAKER_00You just have to know how to pivot the conversation to make the risk feel tangible to the client. I use a very specific approach to open their eyes. Let me ask you something. What would it cost you if you had a three-day hospital stay right now? Pause. Here's what most people do not know about their plan.

SPEAKER_01That slight pause is everything. You are forcing them to actually mentally calculate the thousands of dollars they are risking on their current advantage plan. And again, you do not have to figure this out alone. PSM Brokerage has the exact contracting support you need for hospital indemnity and all these ancillary lines to help you build this exact stack. You can lean on their product specialists to find the most competitive riders in your specific zip code.

SPEAKER_00But you know, there is a massive clock ticking on all of this, which brings us to the most urgent part of this entire discussion. You cannot wait for a client to get sick to offer this high deductible G combination.

SPEAKER_01No, you really cannot. This is what we call the 90% problem.

SPEAKER_00It is a huge problem.

SPEAKER_0190% of Medicare Advantage enrollees ages 65 and older do not have guaranteed issue rights to purchase a Medigap policy if they decide to leave their advantage plan outside of the initial 12-month trial period. Right. We are talking about 22.4 million people who might be permanently locked out of Medigap if they wait too long to make the switch.

SPEAKER_00A lot of clients assume they can just switch back to Medigap whenever they want during the annual enrollment period. But the federal guaranteed issue protections are incredibly narrow.

SPEAKER_01Very narrow.

SPEAKER_00They basically only apply if an advantage plan completely terminates coverage in your specific area or if you are still inside that first 12-month trial period. Right. Or if the advantage plan commits actual fraud.

SPEAKER_01That is basically it.

SPEAKER_00Right. If your client does not fit into one of those tiny regulatory boxes, Medigap insurers can and will deny them based on their medical history.

SPEAKER_01And they absolutely do. You look at these insurer applications and the language is brutally clear.

SPEAKER_00Oh, it is.

SPEAKER_01We are talking about deniable conditions like Alzheimer's disease, asthma, cancer, congestive heart failure, diabetes with complications, end stage renal disease, high blood pressure, stroke, I mean, even just basic limitations of daily activities.

SPEAKER_00Yes, exactly.

SPEAKER_01They literally print on the form if the client answers yes to any of these health questions, do not even submit the application.

SPEAKER_00And when you look at the prevalence data, the statistical urgency becomes undeniable. Among all Medicare beneficiaries, 67% have hypertension. Wow. Yeah. 26% have diabetes, 19% have chronic kidney disease, 12% have heart failure, 10% have prostate cancer.

SPEAKER_01Think about what those numbers actually mean for you as an agent sitting at a kitchen table. The vast majority of your long-term advantage clients will be medically unqualifiable by the time they actually feel the pain of their network restrictions and ask you to switch them.

SPEAKER_00Yes. The conversation has to happen before the hospitalization, not after. Once common conditions like hypertension or diabetes progress into complications, they are permanently locked into the advantage system.

SPEAKER_01Now your geography plays a huge role in how you tackle this problem. State protections vary significantly, and those variations create specific opportunities for agents who know the local rules.

SPEAKER_00Right. Like there are four continuous guaranteed issue states, that is, Connecticut, Massachusetts, Maine, and New York. In those states, insurers have to offer continuous or annual guaranteed issue for all Medicare beneficiaries 65 and older, completely, regardless of their medical history.

SPEAKER_01And we are seeing legislative movement and other states to expand these rights. Minnesota, for example, is adding a new guaranteed issue window for beneficiaries ages 65 to 70.

SPEAKER_00Oh, that is right.

SPEAKER_01That new rule becomes effective August 1st, 2026, and it is a one-time use during the Medicare open enrollment period.

SPEAKER_00Aaron Powell Then you have the nine birthday rule states, that is California, Idaho, Illinois, Kentucky, Louisiana, Maryland, Nevada, Oklahoma, and Oregon.

SPEAKER_01Got it.

SPEAKER_00If you are an agent in one of those states, your existing Medigap holders are allowed to switch to an equal or lesser plan within 30 to 63 days of their birthday, depending on the state, without any medical underwriting.

SPEAKER_01If you are in a birthday rule state, you have a built-in recurring calendar for these reviews. Every month, you have a roster of clients you can call to improve their coverage. But if you are writing business everywhere else, you have to initiate this proactively. You have to build the evidence and have the conversation right now to protect your client's coverage and to protect your own book of business.

SPEAKER_00Because if you do not, someone else will. Or the client will get sick and be stuck blaming you for their out-of-pocket bills.

SPEAKER_01To understand where the specific targets are in your existing book, it helps to understand where the market is currently sitting. Right now, Plan G holds 39% of all Medigap enrollment. Plan N holds 10%.

SPEAKER_00And then you have the sleeping giant, which is Plan F. Plan F still holds 36% of the entire market. But remember, Plan F has been completely closed to anyone newly eligible for Medicare since January 1st, 2020.

SPEAKER_01That brings us to a really important strategic reality for you to consider right now. Together, Plan G, Plan F, and Plan N represent 85% of all Medigap enrollees. But look closely at that massive Plan F block.

SPEAKER_00It is massive.

SPEAKER_01It holds 36% of the market, but it is aging rapidly, and the pool is shrinking because absolutely no new healthy entrants can join the plan. Without new, healthy people coming in to offset the medical claims of the older members, those plan F premiums are mathematically destined to climb significantly in the coming years. Without a doubt. So here's the question you need to ask yourself as an agency owner. Who is running CRM reports right now to re engage those specific Plan F clients and move them to a high deductible G option before a competing agent dials their number?

SPEAKER_00That is this episode of the Insurance Producers Guild. If you are not already with PSM Brokerage, this is the kind of product intelligence our agents get. Talk to us about contracting.