The Insurance Producers Guild

The Insurance Producers Guild is a strategic briefing for insurance professionals, focused on Medicare, ACA, life insurance, and the evolving insurance landscape. Each episode distills complex industry changes into clear, practical intelligence.

The Insurance Producers Guild

EP11 CMS, AI, and the Agent Squeeze of 2027

Use Left/Right to seek, Home/End to jump to start or end. Hold shift to jump forward or backward.

🎙️ Episode Description

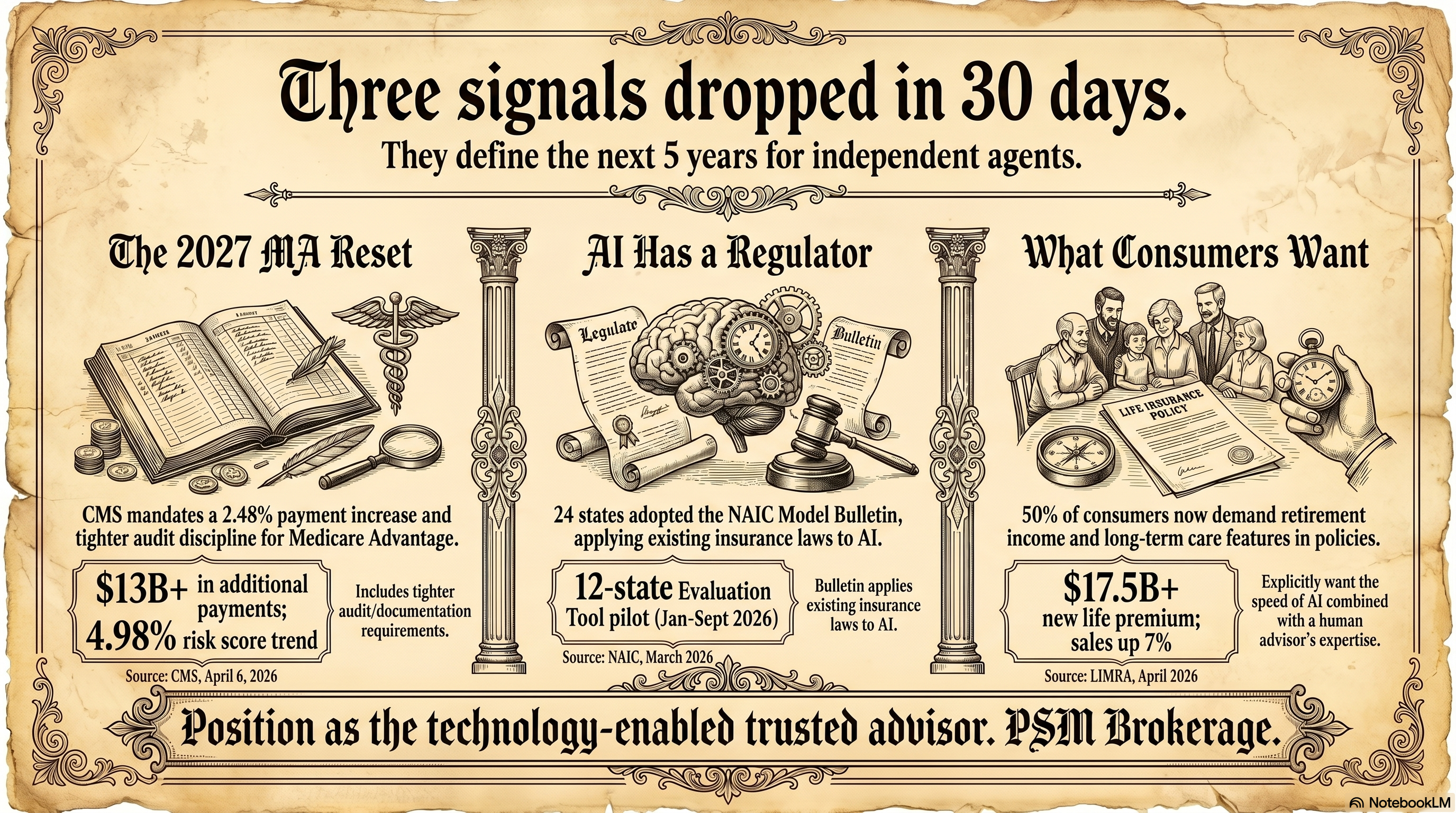

Three major industry signals dropped within 30 days — and they point directly at how independent agents will need to operate over the next five years.

The Centers for Medicare & Medicaid Services finalized 2027 Medicare Advantage payments with a 2.48% increase, paired with tighter audit and risk score controls. The National Association of Insurance Commissioners confirmed states will lead AI regulation, with adoption already underway. And LIMRA data shows consumers want both digital speed and human advice.

This episode breaks down what to say about AI, how to reposition life insurance using living benefits, and why retention is becoming the highest-leverage move heading into 2027.

🔑 Key Topics Covered

- 2027 Medicare Advantage payment increase + tighter oversight

- State-led AI regulation and NAIC model adoption

- LIMRA data: digital + human advisor demand

- Handling AI/chatbot objections in sales conversations

- Retention and living benefits positioning strategies

🎯 What This Means for Agents

- Compliance and documentation matter more as oversight tightens

- AI won’t replace agents — but it will reshape expectations

- Your role shifts to advisor, not just information source

- Retention activity will outperform pure new sales

- Clear client education (especially living benefits) is a differentiator

🔗 Sources

- CMS 2027 Medicare Advantage and Part D Rate Announcement (cms.gov)

- NAIC Issue Brief on Artificial Intelligence and State Insurance Regulation (naic.org)

- LIMRA 2026 Insurance Barometer Study (limra.com)

📌 GO-DO (Next 24–48 Hours)

Pick 3 clients with policies older than 24 months and book a 15-minute review.

Use this opener:

"I do a quick annual review with my clients. The industry just shifted, and there are features available now that did not exist when you bought your policy. Can we spend 15 minutes this week so I can show you?"

3 per week = 12 per month. That is your retention system.

Infographic: https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/IPG_EP11_Infographic.png

Slides: https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/IPG_EP11_Slides.pdf

{kind=link}

The Insurance Producers Guild Podcast delivers intelligence for insurance agents looking to stay ahead of industry trends.

Follow the show and connect with PSM Brokerage to access tools, training, and support designed to help you grow your business.

Learn more: https://www.psmbrokerage.com

If you ask any independent insurance agent what their biggest threat is right now, they will probably tell you it's a combination of three things. Trevor Burrus Yeah.

SPEAKER_01I hear it every single day in the field.

SPEAKER_00Trevor Burrus Right. They will say artificial intelligence is coming for their job, or that state regulators are making compliance impossible, or they think tighter Medicare Advantage economics will just, you know, squeeze them completely out of the business. Totally.

SPEAKER_01There is a very real fear out there right now. You can feel it if you're sitting at your kitchen table looking at your agency dashboard.

SPEAKER_00Absolutely. But um that is the exact mission for this discussion. Because when you ignore the headlines and actually look at the data, the reality is the exact opposite.

SPEAKER_01Aaron Powell The exact opposite. Consumers actively want a human advisor. Carriers desperately need agents who retain clients. And regulators are, well, they are aggressively protecting the human in the loop model.

SPEAKER_00It is a massive window of opportunity, not a threat. I have been in this business for over 25 years, and whenever there is a massive industry shift, the noise points to panic, but the data points to profit.

SPEAKER_01Yeah, the agents who position themselves right now as technology-enabled trusted advisors are going to own the next decade and monetize this shift today.

SPEAKER_00Exactly.

SPEAKER_01We have seen this firsthand, you know, through PSM brokerage business coaching. We watch agents successfully lean into this exact strategy to grow their books.

SPEAKER_00Aaron Powell So let us unpack the three forces shaping the next two to five years. We have the 2027 MA rate reset, the new state level AI oversight, and the latest consumer data on what buyers actually want.

SPEAKER_01I love it. Let us start with the MA reset.

SPEAKER_00Right. So looking at the April 2026 CMS rate announcement, the headline numbers actually look fantastic.

SPEAKER_01They do.

SPEAKER_00We are looking at a net average increase of 2.48%. That equals over $13 billion in additional MA payments.

SPEAKER_01Right. And when you factor in the estimated risk score trend, that number jumps to 4.98%.

SPEAKER_00Yeah, which is roughly $26 billion with an effective growth rate of 5.33%. Plus the Part D risk adjustment is also being updated for the Inflation Reduction Act changes.

SPEAKER_01So it sounds like the carriers are getting this massive windfall.

SPEAKER_00It does. But there is always a stricter regime underneath the money. CMS is implementing much tighter discipline. For example, they are explicitly excluding diagnoses from audio-only encounters. Wow. Yeah. And they are also excluding diagnoses from unlinked chart review records, which causes a negative 1.78% impact right there.

SPEAKER_01That is huge.

SPEAKER_00And on top of that, CMS is sticking with the 2024 risk adjustment model.

SPEAKER_01So um it is basically like a bank offering a higher interest rate on your savings account, but they send a strict building inspector to your house before you can withdraw the funds.

SPEAKER_00That is a perfect analogy. The money is there, but the scrutiny is intense. Carriers are facing massive audit pressure.

SPEAKER_01Right. Meaning they will only reward clean enrollment and high retention. Yeah. They need sticky books of business.

SPEAKER_00Exactly. So what is the immediate application for the agent in the field?

SPEAKER_01Well, because carriers need perfectly documented, sticky clients. The play is to preempt the AEP rush right now.

SPEAKER_00Okay. How do we do that?

SPEAKER_01Here's the play I would run. Do not wait for fall. Run mid-year policy reviews now, so your book is documented and sticky before 2027 arrives.

SPEAKER_00Oh, that makes a lot of sense.

SPEAKER_01You sit down, you verify their doctors are in network, check their prescriptions, and document everything. It locks the back door.

SPEAKER_00But doing that manually for a large book of business is, you know, physically impossible.

SPEAKER_01Totally. Which is why you have to utilize the PSM marketing hub. You use the platform to automate and send out these mid-year review invitations to your current Medicare and Life clients.

SPEAKER_00Right. Let the technology do the heavy lifting.

SPEAKER_01Exactly.

SPEAKER_00Which actually brings us perfectly to the second major force, artificial intelligence. Because the moment you bring up AI, agents freeze up.

SPEAKER_01Oh, they panic. They assume state regulators are going to pull their license.

SPEAKER_00Right. But we have the March 2026 NAIC issue brief here. The National Association of Insurance Commissioners officially opposed federal preemption.

SPEAKER_01Aaron Powell Meaning state regulators own the AI oversight.

SPEAKER_00Yes. And about 24 states have already adopted the model bulletin. Plus, there is a 12-state evaluation tool pilot running from January through September 2026.

SPEAKER_01I hear agents say this state-by-state stuff is a nightmare, but it is actually a gift.

SPEAKER_00Aaron Powell How so?

SPEAKER_01Because the existing insurance laws apply to AI just like they apply to humans. The compliance perimeter has not moved an inch.

SPEAKER_00Right.

SPEAKER_01So now that the rules are clear, small but well-documented agencies can safely use AI to compete with massive call centers.

SPEAKER_00Aaron Powell That levels the playing field completely. But um let me ask you this how do you handle a prospect who thinks they do not need an agent because they can just go online and use a generative AI chatbot to pick their plan?

SPEAKER_01I get that objection a lot. Consumers think it's a free shortcut. Right. Here is what I would say word for word. I tell them, I love that you are doing your research, but algorithms are not governed by fiduciary or suitability standards in the same way a licensed agent is.

SPEAKER_00Oh, that is good.

SPEAKER_01Yeah. I say when you work with me, you get governed advice tailored to your life. And it costs you nothing extra. A chatbot cannot advocate for you when a claim gets denied.

SPEAKER_00That is such a powerful pivot. You are moving the value away from just picking a plan to having a governed advocate.

SPEAKER_01Exactly. The contract, just paper until a human forces the carrier to honor it.

SPEAKER_00And as a quick operational mode on that, agents should definitely lean on the PSM compliance and legal department. They can ensure any new marketing tools you adopt meet these clear state guidelines.

SPEAKER_01Absolutely. So we have covered the tighter MA audits and the AI regulation. But what about the end consumer?

SPEAKER_00Yes, the 2026 Limerae insurance barometer. This connects everything together. The U.S. life insurance industry is booming right now.

SPEAKER_01It really is.

SPEAKER_00New annualized premium topped $17.5 billion in 2025, and sales jumped 7%.

SPEAKER_01Aaron Powell But the interesting part is what they are actually buying.

SPEAKER_00Aaron Powell Right. The pattern from Limera is striking. Exactly half of consumers want policies that create retirement income.

SPEAKER_01Half want long-term care coverage.

SPEAKER_00Yep. Half want critical illness coverage, and half want emergency funds. Plus, they want customization based on life events.

SPEAKER_01Aaron Powell So they are totally rejecting the old strictly death benefit approach.

SPEAKER_00Aaron Ross Powell Exactly. And the punchline from Limera is that consumers appreciate digital advances, but they yearn for human connection. Trevor Burrus Yeah.

SPEAKER_01They want technology to make the process faster, but they want the advisor to guide them.

SPEAKER_00Aaron Powell The human advisor is the durable asset here.

SPEAKER_01Aaron Ross Powell And you know, an informed buyer actually means a shorter close. They already know they have a problem. They just need you to validate the solution.

SPEAKER_00Aaron Powell Which makes the agent a more valuable advisor. But since consumers want living benefits, you have to pivot your approach.

SPEAKER_01Aaron Powell Well, you have to. If you sit down and just pull out a final expense rate sheet, you will lose the room. Right. Let me give you the script I use for a living benefits opener. It reframes life insurance from a death benefit to financial flexibility.

SPEAKER_00Let us hear it.

SPEAKER_01When we sit down, I say, most people think this is just a check for your family on your worst day. But the modern policies we are looking at are actually financial Swiss Army knives.

SPEAKER_00I love that phrase.

SPEAKER_01Thanks. I tell them, we can customize this to build retirement income, cover long-term care, or act as an emergency fund while you were still alive. Which of those is your biggest priority today?

SPEAKER_00Wow. Asking them to choose their priority right out of the gate is incredibly strong. It assumes the sale and gets them dreaming about flexibility.

SPEAKER_01It changes your entire posture. You become an architect customizing a solution, not just someone pushing a commodity.

SPEAKER_00Well, this has been an incredible discussion. We started by dissolving the fear that independent agents are being squeezed out.

SPEAKER_01Right. The data proves it is the opposite.

SPEAKER_00Exactly. We saw that tighter CMS audits mean carriers need perfectly documented, sticky business from agents. We saw that state regulators placed a firm perimeter around AI so you can use it safely.

SPEAKER_01And Limerae data proves consumers want humans to help them navigate these complex living benefits.

SPEAKER_00It all points to the independent agent being elevated, not replaced. So I want to leave you with a final provocative thought to mull over. Go for it. While the industry fixates on the speed of algorithms and the pressure of new MA rates, the ultimate competitive advantage over the next five years is simply the trust you build. Code can calculate risk, but it cannot sit across the kitchen table and provide peace of mind. Your humanity is your greatest business asset.

SPEAKER_01That's this episode of the Insurance Producers Guild. Stay tuned for the next episode. If you're not already with PSM Brokerage, this is the kind of actionable intelligence our agents get. Talk to us about contracting.