The Insurance Producers Guild

The Insurance Producers Guild is a strategic briefing for insurance professionals, focused on Medicare, ACA, life insurance, and the evolving insurance landscape. Each episode distills complex industry changes into clear, practical intelligence.

The Insurance Producers Guild

EP13 The Part D Reset - Fewer Plans, New Rules, Bigger Opportunities

Use Left/Right to seek, Home/End to jump to start or end. Hold shift to jump forward or backward.

🎙️ Episode Description

Episode 13 explores one of the biggest Medicare shifts heading into 2026: fewer standalone Part D plans and continued growth in prescription coverage inside Medicare Advantage plans.

We break down what agents need to know about formulary fit, pharmacy networks, premium trade-offs, and total annual exposure, and why these conversations matter more than ever.

The episode also covers the CMS backdrop behind these changes and shares an annual review approach designed to improve retention, build trust, and uncover compliant opportunities.

🔑 Key Topics Covered

- 2026 Part D changes and fewer standalone plan options

- Medicare Advantage prescription coverage trends

- Formulary, pharmacy, and annual cost exposure reviews

- Annual review strategies for retention and referrals

🎯 What This Means for Agents

- Drug-plan reviews become more important as choices narrow

- Cost conversations extend beyond premiums

- Better reviews can improve retention and referrals

- Compliance-first reviews may uncover additional needs

Infographic: https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/IPG_EP13_Infographic.png

Slides: https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/IPG_EP13_Slides.pdf

{kind=link}

🔗 Sources

CMS Medicare Part D Program Information:

https://www.cms.gov/medicare/prescription-drug-coverage/prescriptiondrugcovgenin

Medicare Plan Finder:

https://www.medicare.gov/plan-compare/

CMS Medicare Advantage & Part D Information:

https://www.cms.gov/medicare/health-drug-plans

PSM Brokerage:

https://psmbrokerage.com

The Insurance Producers Guild Podcast delivers intelligence for insurance agents looking to stay ahead of industry trends.

Follow the show and connect with PSM Brokerage to access tools, training, and support designed to help you grow your business.

Learn more: https://www.psmbrokerage.com

What if I told you that uh in 2026, seeing your Medicare client's premium actually drop might be the absolute worst financial news they get all year.

SPEAKER_00I mean, it sounds completely backwards, right? Because in almost any other industry, a lower monthly bill is a huge cause for celebration. Oh, absolutely. But you know, when you look at the actual mechanics of the healthcare market right now, that dropping premium is often masking this uh this massive transfer of cost risk directly onto the consumer.

SPEAKER_01Yeah, it's a trap. And welcome to this deep dive. Look, if you are joining us today, whether you're an independent insurance agent trying to protect your book of business or, well, just someone fascinated by how this healthcare market actually works, you are in the exact right place. Totally. I've been in the Medicare and Life space for over 25 years. I've seen the PDP launches, the formulary shakeups, all of it. I'm always looking at what these changes mean for the agent in the field. Trevor Burrus, Jr.

SPEAKER_00Right. And I've been at this just as long. Started knocking doors for life insurance, now I run a multi-line agency. And my focus is always uh turning this confusing product stuff into simple talk tracks that actually book appointments and protect your retention.

SPEAKER_01Exactly. So today we are exploring a massive behind-the-scenes transformation happening right now in the 2026 Medicare Part D landscape. We're uh we're pulling from KFF's 2026 enrollment reports and the CMS final rule from April 2026.

SPEAKER_00Aaron Powell And our mission here is really just to give you the plain English version of all this. We want to dissolve that fear you might have of sounding fuzzy when a client asks, you know, why did my plan change or why are there fewer choices?

SPEAKER_01Aaron Powell Right, because agents who can explain this cleanly, they're the ones who will keep the business. So, okay, let's unpack this. We have to start with just the sheer scale of the playing field.

SPEAKER_00Aaron Powell The numbers are wild this year.

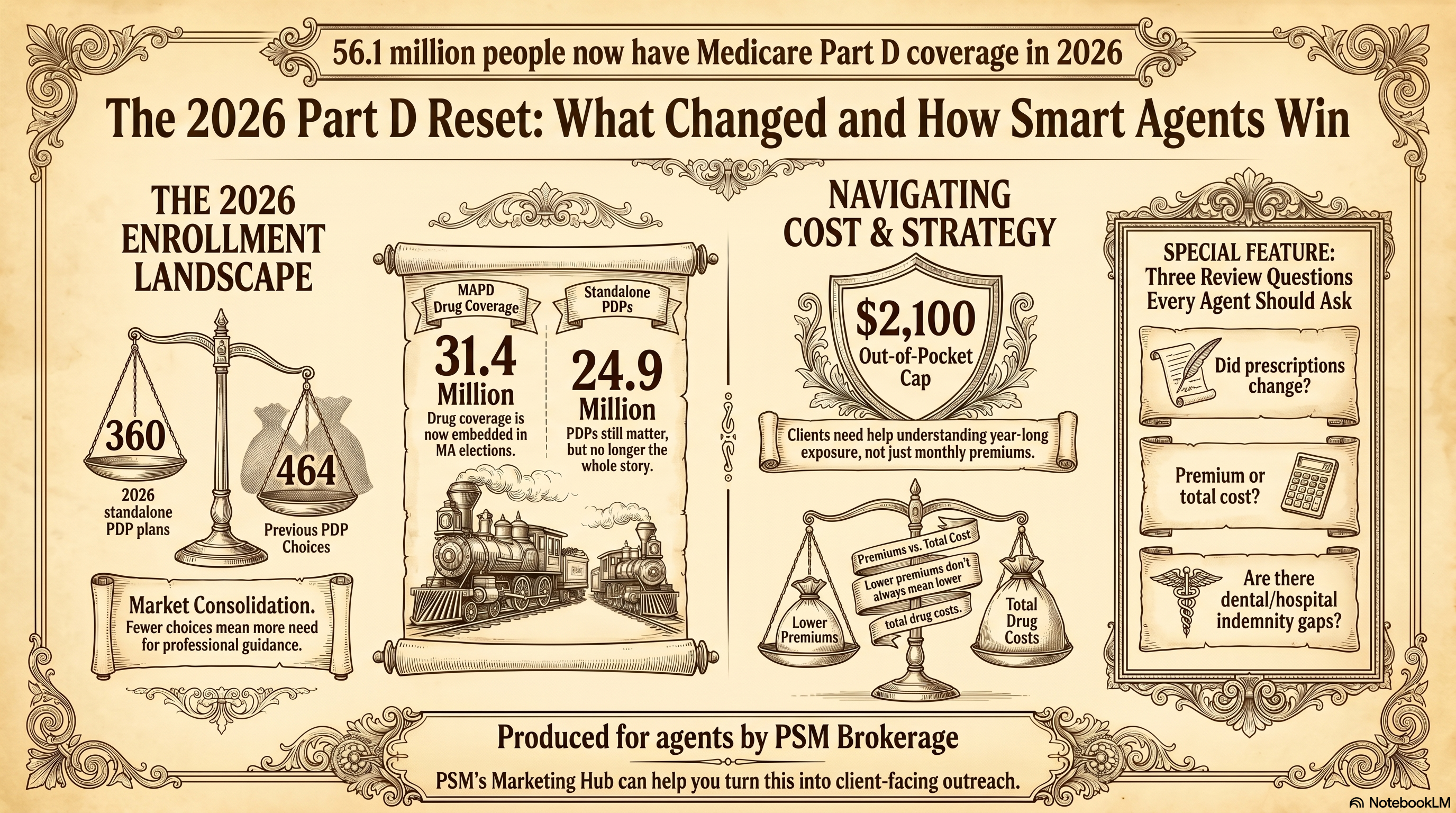

SPEAKER_01They really are. Total Medicare Part D enrollment has hit a staggering 56.1 million beneficiaries for 2026.

SPEAKER_00Aaron Powell That is just a massive slice of the population.

SPEAKER_01Aaron Powell It's huge. But the real story is uh how that population is dividing itself up. Out of that 56.1 million, you've got 31.4 million people enrolled in Medicare Advantage prescription drug plans.

SPEAKER_00Right. The MAPD bundle.

SPEAKER_01Exactly. And meanwhile, the standalone prescription drug plan market, the uh the PDPs, that has shrunk to 24.9 million. Aaron Ross Powell, Jr.

SPEAKER_00Which means the center of gravity has definitively shifted. I mean, for over two decades, standalone PDPs were basically the bedrock of drug cover.

SPEAKER_01Oh, for sure. It was the standard play in the fields, set them up with a med supp, pair it with a standalone PDP, and you're done.

SPEAKER_00Right. But that 31.4 million in MAPD shows us that drug coverage isn't this isolated all-apart purchase anymore.

SPEAKER_01But wait, let me just challenge that assumption for a second. We're still talking about nearly 25 million people in standalone plants.

SPEAKER_00Yes, it's true.

SPEAKER_01So why are we acting like the PDP market is dying? I mean, 25 million consumers is still a massive economy for any agent.

SPEAKER_00Well, the market isn't vanishing overnight, but the business model sustaining it is under severe distress. Because, you know, as more healthy people migrate toward the all-in-one convenience of MAPD, the standalone plans are left with adverse selection.

SPEAKER_01Right, the risk pool gets sicker.

SPEAKER_00Exactly. The people staying in standalone PDPs tend to take more expensive drugs. So the carriers are feeling immense financial pressure to restructure. It means treating an annual drug plan review as some uh separate 10-minute afterthought, it just leaves immense value on the table.

SPEAKER_01Aaron Powell Yeah, I have seen this pattern before. It's exactly like the evolution of television over the last decade. Standalone PDPs operate like the old premium cable model.

SPEAKER_00Oh, that's a great way to put it.

SPEAKER_01Right. You pay a separate bill just for the sports channel, another one for the movie network. But the MEPD model is the giant streaming bundle.

SPEAKER_00And everyone wants the bundle. One ID card, one system.

SPEAKER_01Yeah, but the danger of the bundle is that if a client's specific, say blood pressure medication gets dropped from the formulary, they can't just swap out the drug plan. They have to evaluate their entire medical package.

SPEAKER_00And that ripple effect is immediate. When drug coverage is embedded inside the broader medical plan, any review conversation you have has to evolve. You have to connect formulary changes, pharmacy networks, and medical fit into one coherent strategy.

SPEAKER_01Which naturally leads us to look at the actual choices left on the shelf for those standalone clients. Moving from that macro 56.1 million down to the reality at the kitchen table.

SPEAKER_00Where it actually matters.

SPEAKER_01Exactly. The standalone market is physically shrinking. In 2025, there were 464 standalone plans available nationwide.

SPEAKER_00And for 2026?

SPEAKER_01KFF reports that number plummeted to just 360.

SPEAKER_00Wow. Over a hundred plans wiped off the board in a single cycle. Gone. I mean, carriers are just consolidating their offerings, merging populations, or just exiting regions entirely because the math doesn't work for them anymore.

SPEAKER_01Yet here is the absolute curveball in the data. At the exact same time that 100 plans disappear, average PDP premiums in many states are actually going down.

SPEAKER_00Which is so counterintuitive.

SPEAKER_01Right. If I am a consumer and I see fewer confusing options and a cheaper monthly bill, I'm thinking this is a huge win. Life is easier.

SPEAKER_00And this is the exact paradox that catches beneficiaries off guard. Look, the headline of a lower premium is a brilliantly disguised trap.

SPEAKER_01How so? Walk us through the mechanics.

SPEAKER_00Well, insurance carriers have a fixed pool of money, right? If regulatory pressures are squeezing their margins, they have to save money somewhere. Makes sense. But raising the monthly premium is highly visible. It makes clients angry, it makes them shop around. So instead, carriers hold the premium flat or they drop it by a few bucks just to keep the consumer sedated.

SPEAKER_01It's the budget airline strategy. You see a round-trip ticket for $29 and you think you stole it.

SPEAKER_00Until you get to the gate.

SPEAKER_01Right, until you realize they're charging $60 for a carry-on, $15 to pick a seat, and $5 for water. Your total cost doubled, but the sticker price looked amazing.

SPEAKER_00That is the exact mechanism happening with 2026 drug plans. The client gets their annual notice of change, they see the premium went from $25 down to $18, and they think, I'm saving money.

SPEAKER_01Meanwhile, the carrier just moved their daily insulin from tier two to tier four.

SPEAKER_00Exactly. Or they drop the independent pharmacy down the street from the preferred network. I mean, a $7 drop in premium means literally nothing if the copay at the counter just jumped by $80 a month.

SPEAKER_01So when we look at what top agencies are doing right now, they don't wait for the client to fall into that trap. They attack the misconception head on.

SPEAKER_00Write this down because this is how you handle it. You have to anticipate the objection before they even say it.

SPEAKER_01Okay, let's role play. I'm the client. I call you up and say, hey, my plan lifts cheaper next year. My premium actually went down, so I really don't think we need to meet.

SPEAKER_00Right. An amateur agent just agrees, takes the easy win, and hangs up. But the professional validates the relief and pivots to the hidden risk.

SPEAKER_01What's the exact phrase?

SPEAKER_00You say, I am so glad your premium went down, John. That is a great baseline. But we are seeing a massive trend this year where carriers lower that monthly premium while quietly changing which pharmacies are preferred and bumping specific medications to higher tiers.

SPEAKER_01Oh, that's good. It introduces doubt right away.

SPEAKER_00Exactly. Then you close with: My job is to make sure your lower premium isn't hiding a surprise $50 jump in your actual pharmacy costs. Grab your pill bottles and let's run a quick 10-minute diagnostic just to be safe.

SPEAKER_01I love that word, diagnostic. Okay. Because it positions you as a clinician, not a salesperson. You are diagnosing their total cost structure.

SPEAKER_00It changes the entire power dynamic of the phone call.

SPEAKER_01But to really understand why carriers are scrambling to shift these costs, we have to look at the new regulatory framework. On April 2nd, 2026, CMS handed down the finalized contract year 2027 rule.

SPEAKER_00The big one.

SPEAKER_01Yeah, the engine driving all this market chaos. It enforces the massive Part D redesign for the Inflation Reduction Act. It streamlines enrollment and updates star ratings.

SPEAKER_00Let's pause on star ratings for a second, because that term gets thrown around a lot in agency meetings. But how does that actually hit the consumer's wallet?

SPEAKER_01Well, think of star ratings as uh like a Yelp review for insurance carriers, but with a billion-dollar bonus attached.

SPEAKER_00A very lucrative Yelp review.

SPEAKER_01Exactly. CMS grades plans from one to five stars. If a plan hits four stars or higher, they get massive bonus dollars from the government. The carriers then use that money to fund extra benefits for the consumer, like lower co-pays or a better dental.

SPEAKER_00Right. So if the new CMS rule tightens the math on how those stars are calculated, which it did, then carriers lose their bonus and they instantly have less money to fund consumer benefits. That's why plan quality can degrade overnight, even if the carrier didn't really do anything wrong.

SPEAKER_01Which brings us to the absolute centerpiece of the redesign. The final rule permanently eliminates the old coverage gap phase. The infamous donut hole. Gone. And it establishes a strict 2026 annual out-of-pocket cap of $2,100.

SPEAKER_00Which is, I mean, it's the most consequential shift in party history.

SPEAKER_01Absolutely. We are moving from a system of totally unpredictable exposure to a hard ceiling. For years, I'd see seniors experience drug costs like this terrifying roller coaster in the dark.

SPEAKER_00Right. They pay a deductible, cruise along with fine copays, and then suddenly hit the donut hole.

SPEAKER_01And the track just drops out from under them. Suddenly they're paying a huge percentage of the retail cost. It was awful because they never knew how bad the drop would be.

SPEAKER_00But this new $2,100 cap acts like a reverse deductible. You climb the ladder of copays, and once you hit $2,100, you hit concrete, the ride stops.

SPEAKER_01The absolute worst case scenario is locked in, which brings incredible psychological relief to the client.

SPEAKER_00It does. The conversation isn't about warning them about the donut hole anymore. It's just about managing cash flow up to that $2,100 mark. But wait, we have to look at the other side of the math here.

SPEAKER_01Who pays the bill?

SPEAKER_00Exactly. If the consumer's risk stops at $2,100, who is paying for the drug us after that?

SPEAKER_01The insurance carrier.

SPEAKER_00Yes. The carrier is suddenly on the hook for this massive catastrophic liability that they didn't have to absorb five years ago.

SPEAKER_01Aaron Powell And there is the hidden causality behind everything we've talked about today. That's why carriers dropped 100 plans. They can't afford the risk.

SPEAKER_00That's why they drop premiums to keep people from shopping while secretly restricting the pharmacy networks and aggressively managing their exposure before the client hits that cap.

SPEAKER_01It connects all the dots perfectly. The rules of engagement are just completely changed. And because of the new CMS enrollment rules, this stuff is highly visible. The mailers are going out, the news is talking about the cap.

SPEAKER_00Clients are confused. They know the rules change, they just don't have the technical vocabulary to understand it.

SPEAKER_01Which means the ability to sit at a kitchen table and translate this CMS rule book into plain English. That is the ultimate competitive advantage for an agent right now.

SPEAKER_00Without a doubt.

SPEAKER_01But the stakes are high. One wrong recommendation could lock a senior into a misaligned $2,100 liability. So how does an independent agent protect themselves? You can't just wing this from memory anymore.

SPEAKER_00No, absolutely not. You have to rely on institutional infrastructure. And this is exactly where organizations like PSM Brokerage are proving their value to the independent agent.

SPEAKER_01Because you cannot operate on an island right now.

SPEAKER_00You need an operational partner. PSM Brokerage provides their agents with access to the marketing hub. So instead of you trying to draft your own flyers explaining the $2,100 cap.

SPEAKER_01Which is a compliance nightmare waiting to happen.

SPEAKER_00Oh, totally. PSM provides pre-built compliant resources designed to communicate the value of the annual review in plain language. Plus, their training and contracting support keeps you updated on the minute details across those 360 remaining standalone plans.

SPEAKER_01The compliance piece is massive. CMS is scrutinizing everything right now. Relying on PSM's legal and compliance teams to review your outreach before a large campaign goes out, that ensures your messaging isn't just effective, but insulated from blowback.

SPEAKER_00Exactly. It lets the agent just focus on the human element rather than panicking over a new CMS marketing mandate.

SPEAKER_01So let's transition to the economics of running these reviews. Because I know, and you know, successful agencies do not survive on Part D commissions alone.

SPEAKER_00The margins just aren't there.

SPEAKER_01Right. So if I'm an agent and I'm deep in the weeds checking a client's specific insulin tiers and their preferred pharmacies, how do I pivot to other products? I don't want to sound like a desperate salesperson and burn the trust I just built.

SPEAKER_00Well, the pivot only feels desperate if it's disconnected from the problem you're solving. The key here is organic discovery.

SPEAKER_01Walk us through that. How does that actually sound in the home?

SPEAKER_00Well, when you do a thorough forensic review of their drug costs, you naturally uncover vulnerabilities in their overall financial armor. So say you just confirmed their drug costs will cap out at $2,100. You simply ask them, John, if you hit this cap by July, are you comfortable absorbing that $2,100 hit from your savings?

SPEAKER_01Oh, and right there they reveal their liquidity.

SPEAKER_00Exactly. They might say, Yeah, we have a CD for medical emergencies. Or they might say, honestly, that would completely wipe out our checking account.

SPEAKER_01So you were diagnosing their broader financial resilience.

SPEAKER_00You got it. And once you know that the transition is seamless, you say, look, we have your drug costs capped, which is great. But looking at your total risk, a five-day hospital stay would still generate thousands in co-pays. If $2,100 is a stretch, a hospital bill could be devastating.

SPEAKER_01That is brilliant. You've naturally opened the door for an ancillary protection, like a hospital indemnity policy, or even a dental plan. If they complain about a root canal, their advantage plan won't fully cover.

SPEAKER_00Exactly. And because you're operating within PSM brokerage's verified product lines, hospital indemnity, life, annuities, ACA, you have access to top-tier carriers to fill those exact gaps.

SPEAKER_01You aren't cross-selling just to inflate a commission check. You're deploying a legitimate solution to a vulnerability you found ethically during a mandated review.

SPEAKER_00And the foundation of that cross-sell is the trust you engineered by expertly navigating their Part D confusion. If you save them from the lower premium trap, they will trust you on a hospital indemnity policy.

SPEAKER_01That is exactly what matters in the field. So let's zoom out and summarize the journey we've taken today. We started with the macro, the landscape shifting heavily toward bundled MAPD coverage with 31.4 million people.

SPEAKER_00While the standalone PDP market contracted down to just 360 plans.

SPEAKER_01Right. We exposed the cost shifting mechanism where carriers drop premiums to keep clients sedated while secretly raising drug tiers to cover their own liabilities.

SPEAKER_00All driven by the CMS contract year 2027 rule that cemented the $2,100 out-of-pocket cap. It's a reverse deductible that helps the consumer but forced huge structural changes on the carriers.

SPEAKER_01And we looked at how top professionals use institutional support from PSM brokerage to safely translate these changes and organically cross-sell. Look, whether you are defending your book of business or just observing the market, the takeaway is clear. Treating drug coverage as an afterthought is a guaranteed path to loosen clients.

SPEAKER_00You are the only barrier between a confused client and a catastrophic surprise. So here is what you need to do in the next 24 to 48 hours.

SPEAKER_01Action time.

SPEAKER_00Pull a list of your top 20 existing Medicare clients. Specifically isolate those in standalone PDPs or those taking expensive medications. Get on the offensive before the carrier's confusing mailers hit.

SPEAKER_01And what's the script when they pick up the phone?

SPEAKER_00Here is exactly what I would say. Hi John, this is your Medicare advisor. I'm calling because the new 2026 rules have officially rolled out and the market fundamentally changed. A lot of plans were removed, and the government redesigned the limits with a new $2,100 cap. I'm setting aside 15-minute blocks next week for my existing clients to run a quick diagnostic on your current prescriptions. My only goal is to ensure your pharmacy is still preferred and you aren't walking into hidden costs. Do you have your pill bottles handy on Tuesday morning, or would Wednesday afternoon be better?

SPEAKER_01That is phenomenal. It establishes authority, mentions the macro changes without the CMS jargon, and you just assume the appointment.

SPEAKER_00You don't ask if they want to meet. You offer a choice of times to run a necessary diagnostic.

SPEAKER_01Turning confusion into appointments.

SPEAKER_00Exactly. And I'll leave everyone with this final thought to mull over. We constantly hear that AI and automated quoting tools are gonna make price comparisons effortless, right? Just click a button.

SPEAKER_01People say it all the time.

SPEAKER_00But when you look at the sheer depth of this 2026 overhaul, the deceptive premium drops, the shifting formularies, the carrier panic, it raises a fascinating paradox. Why does this massive influx of automated data actually make the human element, the trusted advisor who can look a client in the eye and decode the math behind the marketing more indispensable today than at any point in the last 20 years?

SPEAKER_01That is something to think about as you hit the phones this week. Thanks for joining us on this deep dive.