The Insurance Producers Guild

The Insurance Producers Guild is a strategic briefing for insurance professionals, focused on Medicare, ACA, life insurance, and the evolving insurance landscape. Each episode distills complex industry changes into clear, practical intelligence.

The Insurance Producers Guild

EP18 Why Medicare Advantage Star Ratings Fell for 2026

Use Left/Right to seek, Home/End to jump to start or end. Hold shift to jump forward or backward.

📝 Episode Description

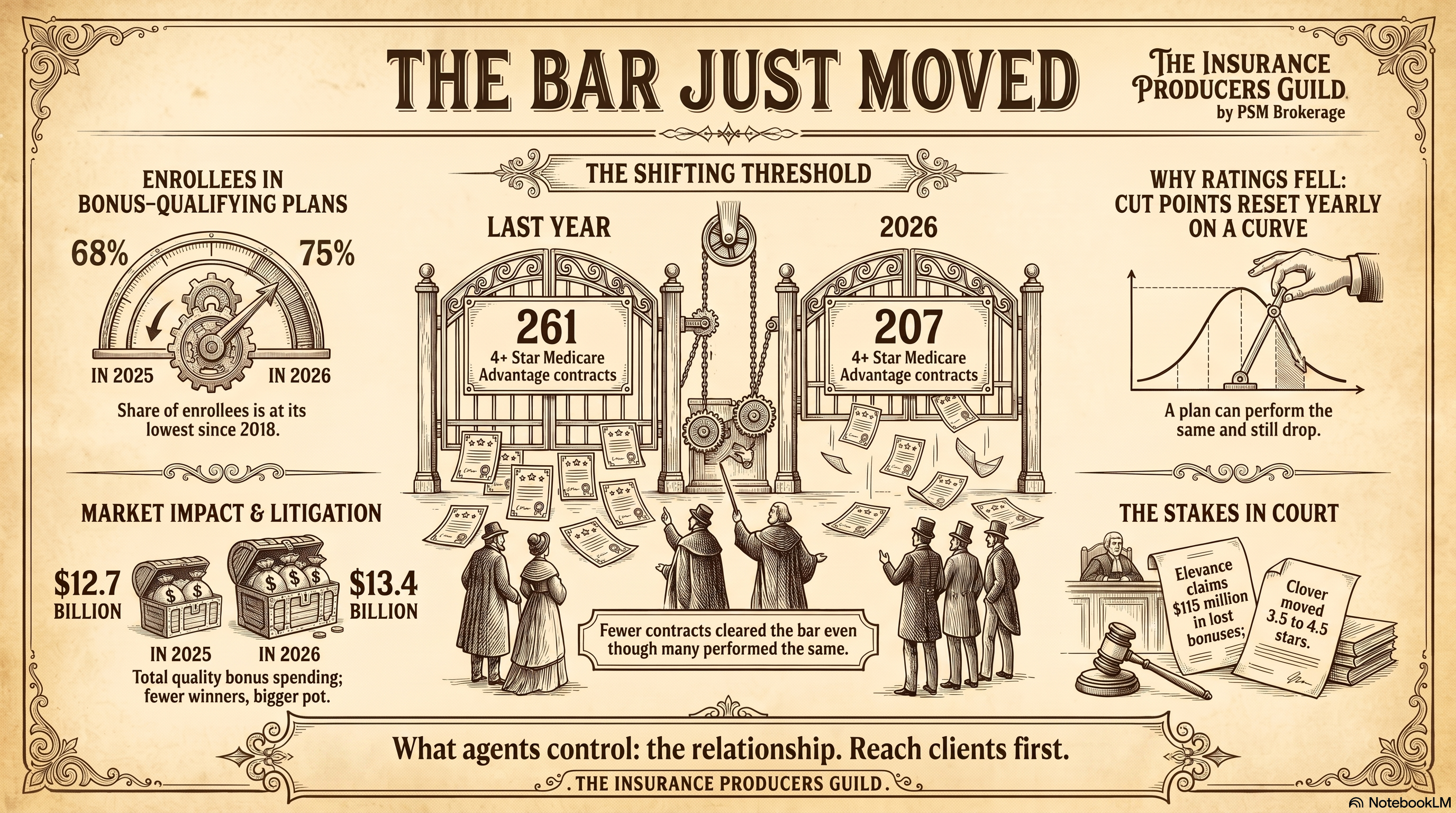

Medicare Advantage contracts earning 4 or more Stars fell from 261 to 207 for 2026, while enrollment in bonus-qualifying plans dropped to 68 percent. Because CMS resets rating cut points annually, a plan can perform similarly and still receive a lower score.

That matters because 4-Star bonuses help support dental, vision, givebacks, and low-premium benefits. Total bonus spending rose to $13.4 billion but is now concentrated across fewer contracts.

The Veteran and The Closer explain the client impact, recent legal challenges involving Clover Health and Elevance, and how agents can review affected business before open enrollment.

🔑 Key Topics Covered

- Why Star ratings can fall

- Annual CMS cut-point changes

- Bonus dollars and plan benefits

- Clover and Elevance legal challenges

🎯 What This Means for Agents

- Lower ratings do not always mean worse performance

- Bonus changes may affect future benefits

- Clients need clear, compliant explanations

- Early outreach can protect retention

🔗 Sources

Quality Bonus Program funding

Medicare Will Spend More Than $13 Billion on the MA Quality Bonus Program in 2026 (KFF, via Medicare Report, July 1, 2026)

Star ratings shift and strategy

Medicare Advantage Star Ratings Are Changing: Is Your Strategy Ready? (mPulse, July 8, 2026)

Elevance lawsuit over star ratings

Elevance Sues CMS Over Star Ratings (MedCity News, Marissa Plescia, July 7, 2026)

📌 GO-DO: Audit Ten Clients

Pull your Medicare Advantage book and flag clients whose plan or contract changed Star ratings for 2026. Schedule ten-minute annual reviews with the first ten clients, using the episode script. Use PSM’s outreach materials and submit your message to Compliance before sending.

Tags: Medicare, Medicare Advantage, star ratings, insurance agents, PSM Brokerage, CMS, enrollment, compliance, quality bonus, retention

Infographic: https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/IPG_EP18_Infographic.png

{kind=link}

Slides: https://www.psmbrokerage.com/hubfs/The%20Insurance%20Producers%20Guild/IPG_EP18_Slides.pdf

The Insurance Producers Guild Podcast delivers intelligence for insurance agents looking to stay ahead of industry trends.

Follow the show and connect with PSM Brokerage to access tools, training, and support designed to help you grow your business.

Learn more: https://www.psmbrokerage.com

If you are looking at your book of business right now, uh, you know, checking out those 2026 Medicare Advantage star ratings, you probably have a familiar pit in your stomach.

SPEAKER_01Yeah. I mean, the fear is completely real. Because if a plan in your book loses its rating, the extra benefits your clients chose could shrink. And honestly, you look like you dropped the ball.

SPEAKER_00Exactly. I have been through this cycle before. I remember back in the earlier days when we saw similar shifts, agents who panicked and just started moving people lost half their book. And I know that panic. But we need to reframe this right now. This is a scoring curve we are dealing with. It is not your failure, and it is not necessarily the plan failing either.

SPEAKER_01Right. And when you understand how that curve works, you know, you become the calm expert in the room for your clients.

SPEAKER_00Aaron Powell So today we are unpacking a whole stack of sources. We have a KFF report from July 2026. We also have a strategic analysis from Impulse and some really eye-opening litigation reporting from MedCity News.

SPEAKER_01Aaron Powell Yeah, our mission today is to figure out why these plan ratings are shifting so wildly and what you actually need to do this week to protect your commissions and your clients.

SPEAKER_00Because if we look at the KFF and MPulse data, the the first thing that jumps out is the money. The overall bonus spending actually rose. It went up to $13.4 billion for 2026.

SPEAKER_01Right, which is up from $12.7 billion. So the pot is bigger.

SPEAKER_00But the bar moved. Only 207 contracts hit four or more stars for 2026. And that is down massively from 261 the year before. Wow. And the enrollee numbers are just as wild. The share of people in those bonus qualifying plans fell to 68%.

SPEAKER_01That is down from 75%, right?

SPEAKER_00Exactly. It is actually the lowest we have seen since 2018.

SPEAKER_01So, you know, you look at those numbers and think the plans just got worse, but the pattern is always the same. These things are graded on a curve.

SPEAKER_00Yeah, I have been through this before. The cut points reset every single year. So a carrier could perform exactly the same. They hit all the same metrics, they answer the phones just as fast, and they still fall below that four-star line.

SPEAKER_01It is literally a moving line. And, you know, when I am talking to my team, I tell them it is really important to keep your language neutral when you talk to clients about carriers. It is not that they suddenly became a bad plan, the whole industry just got pushed to a higher statistical bar.

SPEAKER_00Right, because all the pandemic era guardrails are completely gone now. And CMS changed the weights. The member experience measures dropped from a four times weight down to a two times weight.

SPEAKER_01Oh, wow. So that leverage just vanished overnight.

SPEAKER_00Exactly. Standing still means falling behind. But we need to talk about the actual dollars. Because that bigger pot, that $13.4 billion, is going to fewer winners.

SPEAKER_01Yeah, we have to follow the money here because those bonus dollars are exactly what fund the dental, the vision, the part B give backs, and those low premiums your clients actively shop for.

SPEAKER_00And when a plan drops below four stars, the funding for those extras can just move.

SPEAKER_01It moves and your clients notice. Because when they go to the pharmacy or they try to get a dental cleaning, suddenly it costs more. The KFF report actually brought in some concerns from MedPAC about this whole system.

SPEAKER_00Oh, right. The Medicare Payment Advisory Commission. What did they say?

SPEAKER_01Aaron Ross Powell, they pointed out that the system relies on way too many measures and it completely ignores social risk factors. But the biggest flaw is that they grade at the contract level, not the individual plan level.

SPEAKER_00Great, really. So they just lump everything together.

SPEAKER_01Yeah, exactly. They blend general enrollment plans with special needs plans under one contract. So it masks the true quality of the specific plan your client is actually on.

SPEAKER_00That is like averaging the fuel efficiency of a Sparks car and a city bus, and then using that average to sell a car.

SPEAKER_01It really is. Which is why I am so focused on what we do about it in the field today. When I was starting out door to door, you learned real fast that the first person to speak wins the trust. Stop. Let me give you the script right now. Here's what I would say word for word to get ahead of this.

SPEAKER_00I love this. Let's hear the play.

SPEAKER_01Okay. You pick up the phone and say, hey, I do a quick coverage check with all my clients once a year to make sure nothing changed on your plan. Takes 10 minutes. Can we grab a time this week?

SPEAKER_00That is so simple. But it reaches the client first. It frames it as routine.

SPEAKER_01Exactly. Routine and painless. Only 10 minutes. The impulse data backs this up. They found that members who received proactive outreach before the survey window disenrolled at a rate 2.7 times lower than those who didn't.

SPEAKER_00A 2.7 times lower disenrollment rate? That is huge.

SPEAKER_01Yeah, because if you wait for them to get a confusing letter in the mail or see a commercial, you are already operating defensively. You want to execute this coverage review play immediately.

SPEAKER_00And you know, if you are looking for ways to scale that outreach, PSM Brokerage has some incredible resources for independent agents. Their marketing hub has co-branded annual review outreach materials ready to go.

SPEAKER_01Yeah, and you can always run your client messaging past the PSM compliance and legal department before you mail anything out. And if you need help organizing your book for this, their business coaching team is phenomenal.

SPEAKER_00Right. Because you want to be proactive and you want to do it right. But here's the thing the ground is still moving under our feet. The methodology itself is being contested in court right now.

SPEAKER_01This is the Med City News reporting, right? The Clover Health situation?

SPEAKER_00Yes. Clover Health challenged the CMS methodology in federal court and actually won. A federal judge ruled CMS used the wrong process for 20 quality measures like medication adherence and call center data.

SPEAKER_01They skipped the public rulemaking laws, huh?

SPEAKER_00Exactly. So CMS was forced to recalculate their score.

SPEAKER_01Aaron Powell And they moved Clover from 3.5 all the way up to 4.5 stars, which is a massive jump.

SPEAKER_00Massive. And now Eleven is suing CMS and HHS. They claim they lost $115 million across five of their contracts because CMS refused to give them that exact same recalculation.

SPEAKER_01Wow. $115 million on the line. And that is real money that funds real benefits. So Eleven's wants to be bumped from the three to four star range up to the 3.5 to 4.5 star range.

SPEAKER_00Exactly. They are asking the court to force the math to change, which means ratings can absolutely change after the first publication.

SPEAKER_01So the play I would run right now is patience. Do not panic move a client just based on a scary headline today or a preliminary rating.

SPEAKER_00Right. You have to verify the actual finalized benefits for the coming year first. I have seen agents jump the gun, move a client, and then the original plan ends up restoring the benefits anyway. If a judge steps in, a three-star plan today could magically be a four-star plan tomorrow.

SPEAKER_01And that is why you do the coverage review check. You just tell the client, hey, we are reviewing everything. We're keeping an eye on the shifting math. You are the calm expert guiding them.

SPEAKER_00100%. You let them know that if a benefit changes, it is because the government's scoring curve moved, not because they picked a bad plan.

SPEAKER_01Yeah. That context changes everything for the consumer. It shifts the blame away from you, the agent, and places it squarely on the complex regulatory mechanics.

SPEAKER_00And that is how you protect your book. So just to recap the patterns we found today, the bar moved, not the plans. Billions of dollars are shifting into a smaller group of winners.

SPEAKER_01And the math is literally being fought over in federal court by the major carriers as we speak.

SPEAKER_00Exactly. And the single best defense against all this volatility is proactive outreach. Use that coverage review script to secure your clients.

SPEAKER_01But before we wrap up, I have a thought I want to leave you with. Based on this clover and elements litigation, let's hear it. If major carriers just start successfully suing to recalculate their ratings year after year, does the star rating system eventually become a reflection of a carrier's legal firepower rather than a true measure of actual healthcare quality?

SPEAKER_00Wow. Yeah. If you have the best lawyers, you get the best star rating. That is definitely something we will be watching closely.

SPEAKER_01Yeah, it completely changes how we evaluate these plants.

SPEAKER_00Absolutely. That's this episode of the Insurance Producers Guild. Stay tuned for the next episode. If you're not already with PSM Brokerage, this is the kind of actionable intelligence our agents get. Talk to us about contracting.